Three years ago, I watched a freelance designer friend completely restructure her financial life using what she called her "tripwire budget." She'd been bouncing between $2k months and $8k months for years, always planning for the average that never actually happened. The breakthrough wasn't better budgeting—it was building a system that automatically adjusted based on what was actually happening, not what she hoped would happen.

Most multi-year financial planning breaks because it assumes your income follows a neat upward line. Mine certainly doesn't. Yours probably doesn't either. The standard advice of "save 20% and invest for retirement" falls apart when your income swings by 300% month to month. Or when you're juggling childcare costs while launching a side business. Or when you're deliberately taking a pay cut to switch careers.

What works is building a living financial framework that responds to reality as it unfolds. Not a budget. Not a spreadsheet you update once a year. An operational system with built-in decision rules that tell you exactly when to shift gears.

Why traditional planning fails for variable incomes

The fundamental flaw with conventional financial planning is treating uncertainty as a footnote rather than the main text. Standard templates assume you know your income for the next five years within a reasonable margin. They assume your expenses stay relatively flat. They assume your life circumstances won't dramatically shift.

Real financial lives look different. A freelance photographer might book three weddings one month and none the next. A parent might see childcare costs drop by $1,400 monthly when their kid starts kindergarten, only to pick up afterschool programs and summer camps that eat up the difference. Someone switching from corporate law to teaching sees their income drop by 70% initially, but their stress-related health expenses might disappear entirely.

The mismatch between planning tools and actual life creates a gap where most people just... stop planning. They manage month to month, hoping things work out. The operational overhead of constantly adjusting a rigid plan becomes so exhausting that the plan gets abandoned.

Traditional planning also fails to account for the psychological weight of uncertainty. When you don't know if next month will bring $2,000 or $7,000, committing to fixed savings goals feels impossible. The anxiety of potentially failing to meet those goals often prevents people from setting any goals at all.

The three-scenario framework that actually adapts

Instead of one financial plan, you need three interconnected scenarios running simultaneously. Think of them as different operating modes for your finances, each with its own rules and triggers.

Take charge of your finances with clarity and confidence.

Savioly gives you real-time visibility and actionable steps to improve your money management.

- Automated expense tracking

- Goal-based saving plans

- Personalized financial insights

No credit card required

The lean scenario is your survival mode. This is the minimum viable financial life—rent gets paid, basic food is covered, essential bills are handled. No extras, no savings, just keeping the lights on. For a freelancer in a mid-sized city, this might mean $2,800 monthly. For a two-parent household with young kids, maybe $5,200. The number itself matters less than knowing it precisely.

Your base scenario represents normal operations. Bills are paid comfortably, you're saving something each month, and there's room for occasional discretionary spending. This isn't aspirational—it's what you need to feel financially stable without constant stress. Usually runs about 40-60% higher than your lean scenario.

The stretch scenario is when things are going well. Money is flowing, savings are accelerating, and you can make progress on bigger goals. This is where you fund the emergency account properly, make extra debt payments, or invest in growth opportunities.

| Scenario | Description |

|---|---|

| Lean | The lean scenario is your survival mode. This is the minimum viable financial life—rent gets paid, basic food is covered, essential bills are handled. No extras, no savings, just keeping the lights on. For a freelancer in a mid-sized city, this might mean $2,800 monthly. For a two-parent household with young kids, maybe $5,200. The number itself matters less than knowing it precisely. |

| Base | Your base scenario represents normal operations. Bills are paid comfortably, you're saving something each month, and there's room for occasional discretionary spending. This isn't aspirational—it's what you need to feel financially stable without constant stress. Usually runs about 40-60% higher than your lean scenario. |

| Stretch | The stretch scenario is when things are going well. Money is flowing, savings are accelerating, and you can make progress on bigger goals. This is where you fund the emergency account properly, make extra debt payments, or invest in growth opportunities. |

Each scenario needs complete documentation: exact expense breakdowns, savings rates, discretionary spending limits, and investment contributions. The power comes from having predetermined rules about when to shift between them.

Building trigger points that remove emotion from decisions

The magic happens in the transition rules between scenarios. These triggers need to be specific, measurable, and automatic. No "when things feel tight"—that's how you end up stress-eating ramen for three months while sitting on $8k in savings.

Trigger rules look like this in practice:

Downshift triggers (moving to a more conservative scenario):

-

When checking account balance drops below 2x monthly lean expenses

-

When income trails 3-month average by 30% or more

-

When a major irregular expense is coming within 60 days

-

When client pipeline shows less than 70% of base scenario income for next month

Upshift triggers (moving to a less conservative scenario):

-

When checking account exceeds 3x monthly base expenses for 60+ days

-

When income exceeds base scenario needs for 3 consecutive months

-

When emergency fund is fully funded to target level

-

When all irregular expenses for next 6 months are covered

The specificity matters. "When income is low" isn't a trigger. "When last month's deposits were below $4,200" is a trigger. You can check it, measure it, and act on it without debating whether things are "really that bad" or "probably fine."

Write triggers in exact dollar amounts or timeframes so you can act without debate.

Some people resist this level of structure, thinking it removes flexibility. The opposite is true. Clear triggers give you permission to spend when things are good and permission to cut back when they're not, without the emotional weight of constantly questioning your decisions.

Special frameworks for specific life situations

For Freelancers and Contractors:

Your trigger points need to account for payment delays and seasonal patterns. A wedding photographer might run stretch scenario from May through October, automatically downshift to base in November, and plan for lean scenarios January through March.

Build your triggers around pipeline visibility, not just cash in hand. If you can see four months ahead in your booking calendar, use that forward visibility in your triggers. When booked revenue for the next 60 days drops below base scenario needs, that's your downshift signal—not when your bank account gets low.

Track your "collection lag" religiously. If invoices typically pay 35-40 days after work completion, your triggers need that buffer built in. Your December work pays for February's expenses, so December's pipeline determines February's scenario.

For Parents:

Childcare costs create discrete financial cliffs that standard planning ignores. Your financial scenario might shift dramatically when: a child enters preschool ($800-1500 monthly change), starts public kindergarten ($1000-2000 monthly windfall), needs afterschool care ($300-600 monthly), or requires summer programs ($2000-4000 seasonal hit).

Build separate trigger rules for predictable transitions. Six months before kindergarten starts, begin shifting that preschool payment into a transition fund. When summer break hits, you already have the camp fees covered without dropping to lean scenario.

Consider building "chaos month" provisions into your base scenario. Every parent knows that March brings spring sports registration, May has end-of-year teacher gifts and parties, and September destroys budgets with school supplies and activity sign-ups. Your base scenario should assume one chaos month per quarter.

For Career Shifters:

Your scenarios need time-based evolution built in. Month one after leaving corporate for freelancing might have a lean scenario of $3,500 (because you're draining savings anyway), but month thirteen needs a lean scenario of $4,200 (because emergency funds should be rebuilding).

Create milestone-based trigger adjustments. After landing first three clients, lean scenario increases by 20%. After six months of consistent income, base scenario triggers become less conservative. After one year, stretch scenario includes re-investment in skills and equipment.

Track your "competence curve" financially. As you gain expertise in your new field, your earning potential changes. A new real estate agent might plan for $30k in year one, $55k in year two, and $80k in year three. Your scenarios should evolve with these realistic expectations, not hope for immediate success.

The living document approach (not another dead spreadsheet)

Most financial plans die in spreadsheets that never get opened. A living plan needs to exist where you actually see it and use it. This isn't about perfect tracking—it's about consistent operational awareness.

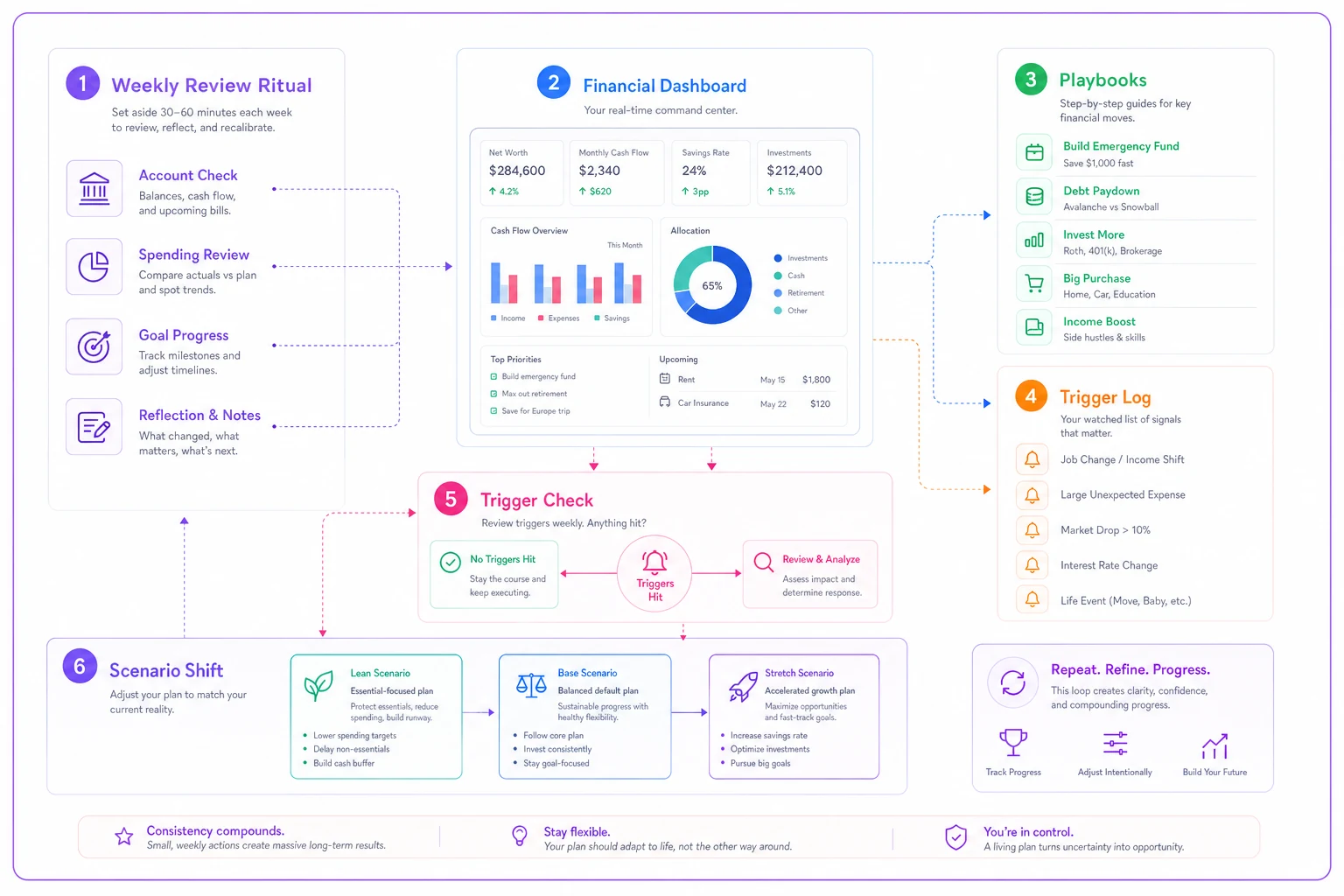

Start with a simple weekly review ritual. Every Sunday morning (or whatever works), you check three things: current scenario status, upcoming trigger points, and any needed adjustments. Takes twelve minutes, not two hours.

Your documentation system needs three components:

The Dashboard: A one-page view showing current scenario, account balances relative to triggers, and next likely transition point. This could be a phone note, a printed page on your fridge, or a bookmark in your browser. The format doesn't matter—accessibility does.

The Playbooks: Detailed instructions for each scenario. When you shift to lean, what bills get paused? What subscriptions cancel? What spending stops? When you hit stretch, what order do you fund goals? Which debts get extra payments first? Document these decisions when you're calm and thinking clearly, not when you're stressed about money.

The Trigger Log: A simple record of when you shifted scenarios and why. This becomes invaluable for refining your triggers over time. Maybe you realize you always upshift too early and end up dropping back to lean within six weeks. That pattern tells you to adjust your triggers.

A simple diagram helps see how the weekly review, Dashboard, Playbooks, and Trigger Log connect.

The system needs regular calibration. Every quarter, review whether your scenarios still match reality. Did lean scenario creep up because you got used to certain conveniences? Did base scenario become bloated with subscriptions you forgot about? Regular tuning keeps the system functional.

Common failure points and their fixes

The first failure point hits around month three, when the novelty wears off and tracking feels tedious. The fix isn't motivation—it's reducing friction. If updating your dashboard takes more than five minutes, it's too complex. Strip it down to the absolute minimum that still provides value.

People also struggle with trigger discipline. You hit a downshift trigger but convince yourself it's temporary, so you ignore it. This breaks the entire system. The fix is making transitions less dramatic. Instead of lean scenario meaning "cancel everything," maybe it means "pause the fun subscriptions but keep the gym." Smaller transitions are easier to execute.

Not accounting for irregular expenses is another common break point. Your car registration, annual insurance payment, or quarterly taxes blow up your carefully planned scenario. Build these into your trigger calculations. If you need $3,000 for taxes in April, start factoring that into your March triggers.

The psychological challenge of downshifting deserves special attention. Nobody wants to tell their family "we're in lean mode this month." Reframe it as operational efficiency. Businesses adjust their operations based on revenue—you're running your household the same way. It's not failure; it's intelligent response to conditions.

Some people get stuck optimizing their scenarios forever without ever implementing them. Perfect scenarios that never get used are worthless. Start with rough numbers, implement the system, and refine based on actual experience. Your first lean scenario might be off by $500—that's fine. You'll calibrate as you go.

Operational improvements through systematic planning

The real power isn't in the planning—it's in the execution clarity it provides. When income drops, you don't panic or debate what to cut. You execute your predetermined lean scenario playbook. When money flows, you don't wonder what to do with it. Your stretch scenario already outlined the priority order.

This systematic approach reduces decision fatigue dramatically. Instead of making 50 small financial decisions monthly, you make one: which scenario are you in? Everything else flows from that choice. The mental energy you save can go toward actually increasing income or optimizing expenses, rather than constantly deciding what to do.

The framework also improves partner communication for couples. Instead of arguing about individual purchases, you discuss which scenario you're operating in. "We're in base scenario, so yes to the new shoes but no to the weekend trip" becomes an operational decision, not a personal judgment.

Over time, patterns emerge that inform bigger decisions. Maybe you notice you spend seven months yearly in lean scenario despite earning decent money. That pattern might reveal that your base scenario is too expensive for your income volatility, or that your client pipeline needs better diversification.

The system creates natural forcing functions for financial progress. When you hit stretch scenario, you're not wondering what to do with extra money—your playbook already designated it for emergency fund growth or debt payment or investment. The automation of good decisions during good times funds your stability during lean times.

For those building businesses or switching careers, the framework provides crucial psychological safety. Knowing you can drop to lean scenario and survive for six months makes taking calculated risks possible. The framework doesn't remove risk—it makes it visible and manageable.

Making the framework work in real households

Implementation starts with brutal honesty about your numbers. Track expenses for one month—not to judge them, but to understand them. Your lean scenario needs to be actually achievable, not aspirational. If you've never spent less than $4,000 monthly, don't set lean at $2,500.

Begin with simple triggers based on bank balance. You can add sophistication later. Starting triggers might be: below $5,000 = lean, $5,000-10,000 = base, above $10,000 = stretch. Run this for three months, then refine based on what actually happened.

Don't try to plan five years out initially. Start with a six-month framework, get it working, then extend the timeline. Most people never get past month one because they're trying to perfect year five. Build the habit first, add complexity later.

Consider seasonal adjustments from the start. If you know December is expensive and January is slow, build those expectations into your triggers. Maybe November automatically triggers saving mode regardless of bank balance, preparing for the known challenges ahead.

The framework should reduce stress, not create it. If checking triggers weekly causes anxiety, switch to biweekly. If three scenarios feel overwhelming, start with two: survival and normal. You can add stretch scenario once the basic system works smoothly.

For households with multiple earners, decide whether you're tracking combined or separate scenarios. Some couples run individual lean/base/stretch scenarios that roll up to household decisions. Others operate purely at household level. Neither is right—pick what creates least friction.

Your money, your rules, your system

Standard financial advice assumes everyone's income looks like a government salary: stable, predictable, gradually increasing. But freelancers, parents, career shifters, and honestly most people under 40 don't live in that reality anymore. Your financial planning system should match your actual life, not some theoretical ideal.

This three-scenario framework with trigger-based rules isn't perfect, but it's functional. It turns the chaos of variable income into a manageable operational system. Instead of constantly wondering if you can afford something, you check which scenario you're in. Instead of stressing about income drops, you execute your downshift playbook. Instead of lifestyle inflation eating every raise, your stretch scenario directs extra money toward actual goals.

Start simple. Define your three scenarios this weekend. Set basic triggers. Run it for a month. Adjust based on what actually happens, not what should happen. Let the system evolve with your life rather than trying to force your life into a rigid system.

Your financial life is an operation you run every single day. Like any operation, it works better with clear procedures, defined trigger points, and predetermined responses to common situations. The framework doesn't make decisions for you—it makes your decisions easier to execute.

The distance between financial stress and financial confidence usually isn't about how much money you have. It's about having a system you trust to handle whatever comes next. Build that system, refine it based on experience, and watch your relationship with money shift from reactive scrambling to operational management.

Start simple. Define your three scenarios this weekend. Set basic triggers. Run it for a month. Adjust based on what actually happens, not what should happen. Let the system evolve with your life rather than trying to force your life into a rigid system.

Ready to master your money?

Join thousands of users leveraging Savioly to build smarter budgets, save more efficiently, and plan for a secure financial future.