Most side-hustlers run their finances backwards. They collect money, spend on supplies, maybe pay themselves something, then scramble during tax season wondering where everything went. The successful ones flip this—they build a side hustle cashflow system from day one that automatically handles taxes, owner distributions, and growth capital before they touch a penny.

The difference between a sustainable side business and one that flames out after eighteen months usually comes down to cashflow discipline. Not passion, not marketing genius, not even product quality. Just boring, predictable money management that keeps the operation running while you're still working your day job.

Why traditional business advice breaks for part-timers

Standard small business finance advice assumes you're all-in. Full-time attention, regular draws, predictable schedules. Side-hustles operate differently—you're reconciling books at 11pm after the kids are asleep, processing invoices during lunch breaks, making purchasing decisions between meetings.

Your operational constraints are different too. You can't spend three hours categorizing expenses or maintaining complex spreadsheets. You need a system that runs mostly on autopilot, catches mistakes before they compound, and doesn't require an accounting degree to maintain.

The cognitive load matters more than most people admit. When you're context-switching between your day job and side business a dozen or more times a week, complex financial systems create friction. Friction leads to procrastination. Procrastination leads to commingled funds, missed quarterly tax payments, and that awful realization in March that you owe $4,800 you don't have.

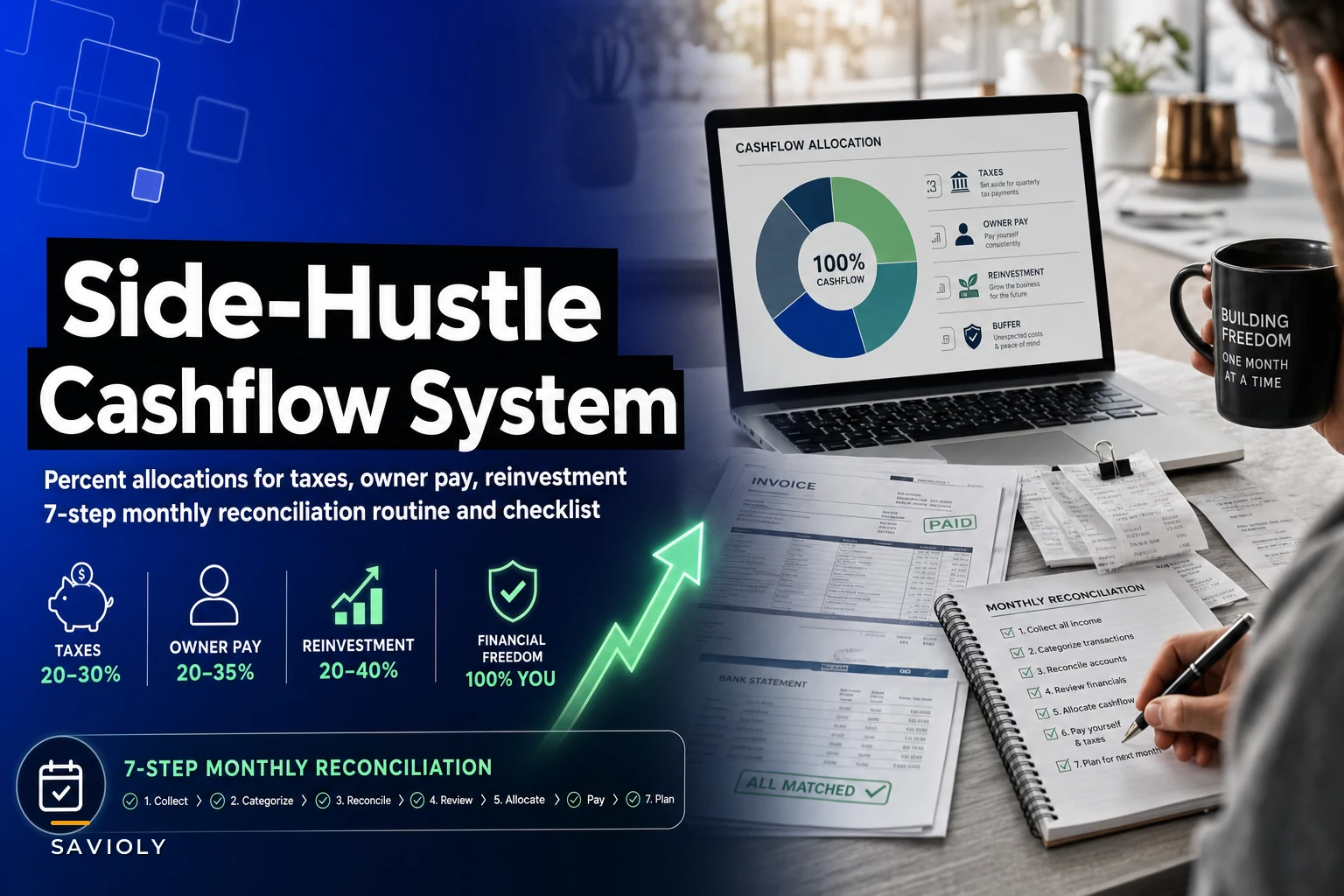

The percentage allocation framework that actually works

Forget complex formulas. A functional side hustle cashflow system needs dead-simple rules you can execute half-asleep. Here's the allocation framework that works across most service-based and product side-hustles earning somewhere between $500 and $8,000 monthly:

Take charge of your finances with clarity and confidence.

Savioly gives you real-time visibility and actionable steps to improve your money management.

- Automated expense tracking

- Goal-based saving plans

- Personalized financial insights

No credit card required

Base Allocation Structure:

-

30% → Tax reserve account

-

35% → Owner pay account

-

20% → Operating expenses account

-

15% → Growth/reinvestment account

These percentages assume you're in the 22–24% federal bracket with standard state taxes. If you're in California or New York, bump the tax reserve to 35%. Texas or Florida with no state income tax, 25% is probably fine.

The key: allocate immediately when money hits your business account. Not weekly, not monthly—immediately. Every Venmo payment, every Stripe deposit, every check. Split it before your brain has time to rationalize why you need "just this one payment" for something urgent.

Setting up four separate accounts sounds excessive until you experience the mental clarity of knowing exactly what's actually yours versus what belongs to the IRS or your business.

Invoice workflows for people with no time

The typical side-hustler invoice flow looks chaotic: email invoices, forget to track payments, scramble to figure out who owes what, accidentally count the same payment twice, realize three months later you never collected from a client.

A stripped-down invoice workflow takes maybe twenty minutes weekly:

The Three-Touch System:

-

Invoice creation (2 minutes per client) - Use the same template every time - Number sequentially (2024-001, 2024-002) - Send immediately after work completion - BCC yourself for records

-

Payment tracking (30 seconds per payment) - Mark paid in your system the moment money arrives - Screenshot/save the payment confirmation - Move the invoice from "pending" to "paid" folder

-

Weekly sweep (10 minutes Sunday evening) - Review all pending invoices - Send friendly follow-up on anything 7+ days old - Flag anything 21+ days for stronger action

Simple tracking table structure:

| Invoice # | Client | Amount | Sent | Due | Paid | Notes |

|---|---|---|---|---|---|---|

| 2024-031 | Johnson Design | $750 | 3/15 | 3/30 | 3/22 | Early payment |

| 2024-032 | ABC Corp | $1,200 | 3/18 | 4/2 | — | Follow-up sent 3/25 |

| 2024-033 | Local Coffee | $400 | 3/20 | 4/4 | 3/21 | Net-15 terms |

This isn't about perfection—it's about having enough visibility to catch problems before they cascade. A client who hasn't paid in 30 days becomes a collections issue. Three unpaid invoices means you need to pause work. Basic operational boundaries that protect your cashflow.

The monthly reconciliation routine that catches everything

Monthly reconciliation for side-hustles isn't about balanced books—it's about catching operational leaks before they sink you. Takes about 45 minutes once a month, usually first Sunday of the month while coffee's brewing.

The 7-Point Monthly Check:

-

Income verification (5 minutes) - Total all deposits to business account - Cross-check against invoice list - Flag any mystery money (yes, this happens)

-

Allocation audit (5 minutes) - Confirm all income got split per percentages - Move any unsplit funds immediately - Adjust if allocation accounts are off

-

Expense category scan (10 minutes) - Group expenses into 5–7 buckets max - Look for surprise recurring charges - Flag anything over $100 for review

-

Tax reserve check (3 minutes) - Calculate

Total income × tax rate - Compare to actual tax account balance - Top up if short (non-negotiable)

-

Pending invoice review (7 minutes) - List all unpaid invoices - Calculate aging (days outstanding) - Mark any for collection action

-

Owner draw decision (5 minutes) - Check owner pay account balance - Decide on distribution amount - Transfer to personal account (or leave it)

-

Next month setup (10 minutes) - Review upcoming expenses - Check growth account for planned purchases - Adjust allocation percentages if needed

A quick visual to map the routine and make the 45-minute sweep feel doable.

This isn't comprehensive accounting—it's operational hygiene. You're looking for patterns, catching mistakes, and making micro-adjustments before small issues become big ones.

Red flags that signal system breakdown

Even simple systems fail when you ignore warning signs. These patterns mean your side hustle cashflow system needs immediate attention:

The mixing spiral: You "borrow" from tax reserves for inventory, planning to replace it next month. Next month you borrow more. By quarter-end, you owe $2,400 in estimated taxes with $300 in the account. This happens faster than people expect—usually complete breakdown within 90 days of the first "borrow."

The growth trap: Your side-hustle hits $5k monthly but you're still running everything through PayPal and a spreadsheet. The operational complexity has outgrown the system but you haven't noticed because you're too busy fulfilling orders. First sign: you start missing invoice follow-ups because there are too many to track manually.

The feast-or-famine whiplash: A big month comes in at $8k, you spend liberally on equipment and marketing, next month drops to $1.5k and you can't cover basic operating expenses. Percentage allocations assume some consistency—wild swings need different rules.

When you spot these patterns, the fix usually isn't complicated. Are you splitting income immediately? Reconciling monthly? Keeping business and personal completely separate? The fundamentals solve most cashflow problems.

Scaling triggers and system upgrades

A functional side hustle cashflow system should carry you from $0 to around $5k monthly. Beyond that, certain triggers indicate you need to upgrade:

When to add complexity:

-

Consistently over $5k monthly for 3+ months

-

More than 15 invoices monthly

-

Multiple revenue streams with different tax treatments

-

Inventory management becomes significant

-

You hire contractors or part-time help

The progression usually looks like:

-

$0–2k/month

Spreadsheet + percentage rules

-

$2k–5k/month

Basic accounting software + bank automation

-

$5k–10k/month

Full accounting platform + monthly bookkeeper

-

$10k+/month

Time to evaluate going full-time

The mistake people make is jumping to complex systems too early. Running QuickBooks for a $500/month side-hustle creates more friction than value. But staying on spreadsheets when you're processing 30 invoices monthly leads to expensive mistakes.

Automation opportunities without overengineering

The temptation with any financial system is to automate everything immediately. But premature automation in side-hustles often creates rigid systems that break when your business model shifts—which happens constantly in the first two years.

Smart automation targets repetitive, error-prone tasks while leaving flexibility where you need it. Invoice generation and payment tracking are good candidates. Strategic decisions about owner draws or reinvestment percentages should stay manual.

Modern operational software can handle the mechanical parts—invoice creation, payment reminders, basic categorization—while you focus on the judgment calls. The better platforms for side-hustlers integrate light AI-assisted automation for categorization and anomaly detection without locking you into rigid workflows.

Think of automation as removing friction, not removing control. You want systems that make the monthly reconciliation take 45 minutes instead of three hours, not systems that hide what's actually happening in your business.

Real scenario: Designer's progression from chaos to clarity

Graphic designer running a side-hustle while working full-time at an agency. Started clean—separate business checking, good intentions about tracking everything. Within six months: personal and business expenses completely mixed, no idea what she owed in taxes, considering shutting down despite steady $3k monthly revenue.

The fix took one weekend. Opened four savings accounts (free with her existing bank), went back through six months of statements to roughly separate business from personal, calculated approximate tax liability, set up percentage splits going forward. Not perfect, but functional.

Monthly routine: 45 minutes, first Sunday of each month. Check deposits against invoices, verify percentage splits happened, scan for weird expenses, make owner draw decision. That's it.

Four months later: $3,400 in tax reserves ready for quarterly payment, consistent $1,000 monthly owner draws, around $1,800 saved toward a new computer setup, zero anxiety about money mixing. The business didn't grow faster or become more profitable. But it became sustainable because she could actually see what was happening.

Why most side-hustles fail at finance

The uncomfortable truth about side-hustle failures: it's rarely about market demand or product quality. Usually it's operational basics. They run out of cash because they spent tax money. They can't invest in growth because they have no idea what's actually profit versus revenue. They burn out from the mental load of never knowing their true financial position.

A side hustle cashflow system isn't about complex accounting or perfect books. It's about creating just enough structure to prevent catastrophic mistakes while maintaining flexibility to adapt. The percentage rules give you guardrails. The monthly reconciliation catches problems early. The invoice workflow prevents revenue leakage.

None of this is revolutionary. But most side-hustlers skip these basics, thinking they'll figure it out when they get bigger. By then, the operational debt has usually compounded beyond recovery. Start with simple systems, maintain them consistently, and upgrade only when clear triggers tell you it's time.

The difference between a side-hustle that survives and one that thrives usually isn't passion or market timing. It's boring, consistent financial operations that protect you from yourself. Set up the system, run it weekly, reconcile monthly. Everything else—growth, scaling, optimization—builds on that foundation.

Ready to master your money?

Join thousands of users leveraging Savioly to build smarter budgets, save more efficiently, and plan for a secure financial future.