Most people arguing about debt payoff strategies miss the actual problem. You've got the avalanche camp calculating interest savings down to the penny, and the snowball crowd preaching quick wins. Meanwhile, real people switch strategies every few months, restart their plans, and wonder why nothing sticks.

Both methods fail because they assume you'll execute perfectly. A hybrid approach works better because it acknowledges what actually happens — you need mathematical optimization when you're motivated and psychological wins when you're not.

The switching problem nobody talks about

Someone with $42,000 in debt across six accounts starts with avalanche because the math checks out. They attack their 24.9% credit card while making minimums on everything else. Three months in, they've barely dented the $8,400 balance. Meanwhile, the car loan is visibly dropping from minimum payments alone. Frustration kicks in.

So they switch to snowball. They pay off the $650 medical bill. Victory. Then the $1,200 personal loan. Another win. But after clearing those, the credit card interest is still bleeding them. Back to avalanche.

This switching pattern destroys progress. Not because either method is wrong, but because switching itself costs momentum. Every restart means recalculating, reorganizing, and losing weeks of focused execution.

Building decision rules that stick

A functional hybrid system needs clear triggers — not vague ideas like "switch when frustrated," but actual numeric thresholds you commit to before emotions enter the picture.

Take charge of your finances with clarity and confidence.

Savioly gives you real-time visibility and actionable steps to improve your money management.

- Automated expense tracking

- Goal-based saving plans

- Personalized financial insights

No credit card required

Start with rate thresholds. Any debt above 20% APR gets avalanche treatment regardless of balance. Most credit cards, payday loans, predatory lending — the interest damage at these rates overwhelms any psychological benefit from clearing smaller debts first.

For everything under 20%, size matters. Debts under $1,000 get snowball treatment if you can eliminate them within two months. This creates quick wins without sacrificing meaningful interest savings. Between $1,000 and $5,000, apply a timeline rule — if you can clear it in six months, snowball works. Otherwise, sort by interest rate.

Above $5,000, pure math takes over unless you hit a motivation crisis. Define that crisis clearly before it happens: missing two scheduled extra payments, avoiding your debt spreadsheet for two weeks, or feeling genuinely avoidant about your finances. These triggers allow temporary snowball pivots without making the switch feel like failure.

The monthly execution framework

Month one is just assessment. List every debt with balance, minimum payment, and interest rate. Calculate your debt-free date under pure avalanche and pure snowball. The difference tells you exactly what flexibility costs.

Say you've got:

-

Credit card

$7,800 at 22.9%

-

Car loan

$14,200 at 6.2%

-

Student loan

$23,000 at 4.8%

-

Medical bill

$450 at 0%

-

Store card

$1,100 at 26.9%

Your attack order becomes:

-

Store card (high rate, clearable in 2–3 months)

-

Medical bill (psychological win, no interest penalty)

-

Credit card (highest remaining rate)

-

Car loan (moderate rate)

-

Student loan (lowest rate)

Months two through four focus on the store card with every extra dollar while maintaining minimums elsewhere. Say you're paying roughly $280 monthly across minimums, plus throwing an additional $400 at the store card. Three months later, it's gone.

Month five pivots to the medical bill. Even though it carries no interest, clearing it frees mental space and rolls that minimum payment forward. Two debts eliminated in five months — momentum is real at this point.

Months six through eighteen attack the credit card. This is the marathon phase. The early wins carry you through a larger balance. You're now throwing $450 extra at this card — your original $400 plus freed-up minimums from cleared debts.

Below is a rough look at how this sequence plays out across the first year:

| Month | Target Debt | Extra Payment | Running Debts Cleared |

|---|---|---|---|

| 1 | Assessment | — | 0 |

| 2–4 | Store card ($1,100 @ 26.9%) | $400/mo | 0 → 1 |

| 5 | Medical bill ($450 @ 0%) | $425/mo | 1 → 2 |

| 6–18 | Credit card ($7,800 @ 22.9%) | $450/mo | 2 → 3 |

| 19+ | Car loan → Student loan | Snowballed amount | 3 → 5 |

Below is a rough look at how this sequence plays out across the first year:

Amortization reality check

Most people underestimate how front-loaded interest affects payoff timelines. On a $7,800 credit card at 22.9%, your first $300 payment includes roughly $149 in interest. Only $151 hits principal. Six months later, the same $300 payment puts $182 toward principal. The acceleration is real but slow to start.

This is exactly why hybrid strategies work. You need those early psychological wins to survive the months where most of your payment disappears to interest. Watching $1,100 completely vanish while simultaneously seeing your credit card drop from $7,800 to $7,200 creates the kind of motivation that actually sustains 18-month payoff plans.

The mathematical purists will show you spreadsheets proving you save $1,847 following strict avalanche over strict snowball. What they won't show you is how many people abandon pure avalanche within six months because the slow progress grinds them down.

Behavioral triggers that actually work

Motivation crises are predictable. They tend to hit around the three-month mark, during major life stressors, or when a large unexpected expense shows up. Build your triggers around these patterns.

The three-month pivot rule: Every third month, you're allowed to clear your smallest remaining debt regardless of interest rate, as long as it's under $2,000. This scheduled pressure release prevents spontaneous strategy abandonment.

The stress override: During job loss, medical emergencies, or major relationship stress, automatically switch to minimum payments plus $50 on your smallest debt. This keeps you moving without overwhelming depleted mental resources.

Schedule your three-month pivot on your calendar the day you start the plan so it's not a decision under stress.

The windfall allocation: Any unexpected money — tax refunds, bonuses, gifts over $500 — gets split 70/30. Seventy percent goes to highest-rate debt, thirty percent to smallest balance. Hybrid on windfalls. Mathematical optimization plus psychological reward.

When pure strategies make sense

Sometimes the hybrid approach adds unnecessary complexity. If your total debt is under $10,000 across fewer than four accounts, just pick one strategy and execute. The optimization gap is minimal, and overthinking the approach becomes its own form of procrastination.

If all your rates cluster within 5% of each other — say everything sits between 18% and 23% — pure snowball often wins. The interest savings from avalanche become marginal while the psychological boost from clearing accounts stays substantial.

On the other end, if you're dealing with genuinely predatory debt — payday loans at 400% APR, title loans at 300% — abandon everything else and attack those first. No psychological win justifies paying those rates a day longer than necessary.

The compound effect of freed minimums

This part gets underestimated. That $650 medical bill might only carry a $25 monthly minimum, but once cleared, that $25 joins your attack fund. Clear three small debts with $25, $35, and $40 minimums, and you've gained an extra $100 monthly without changing your budget at all.

You might sacrifice $200 in interest savings by clearing small debts early, but you gain $100 in monthly firepower that compounds across your remaining payoff period. Run the full calculation honestly and hybrid often comes out ahead.

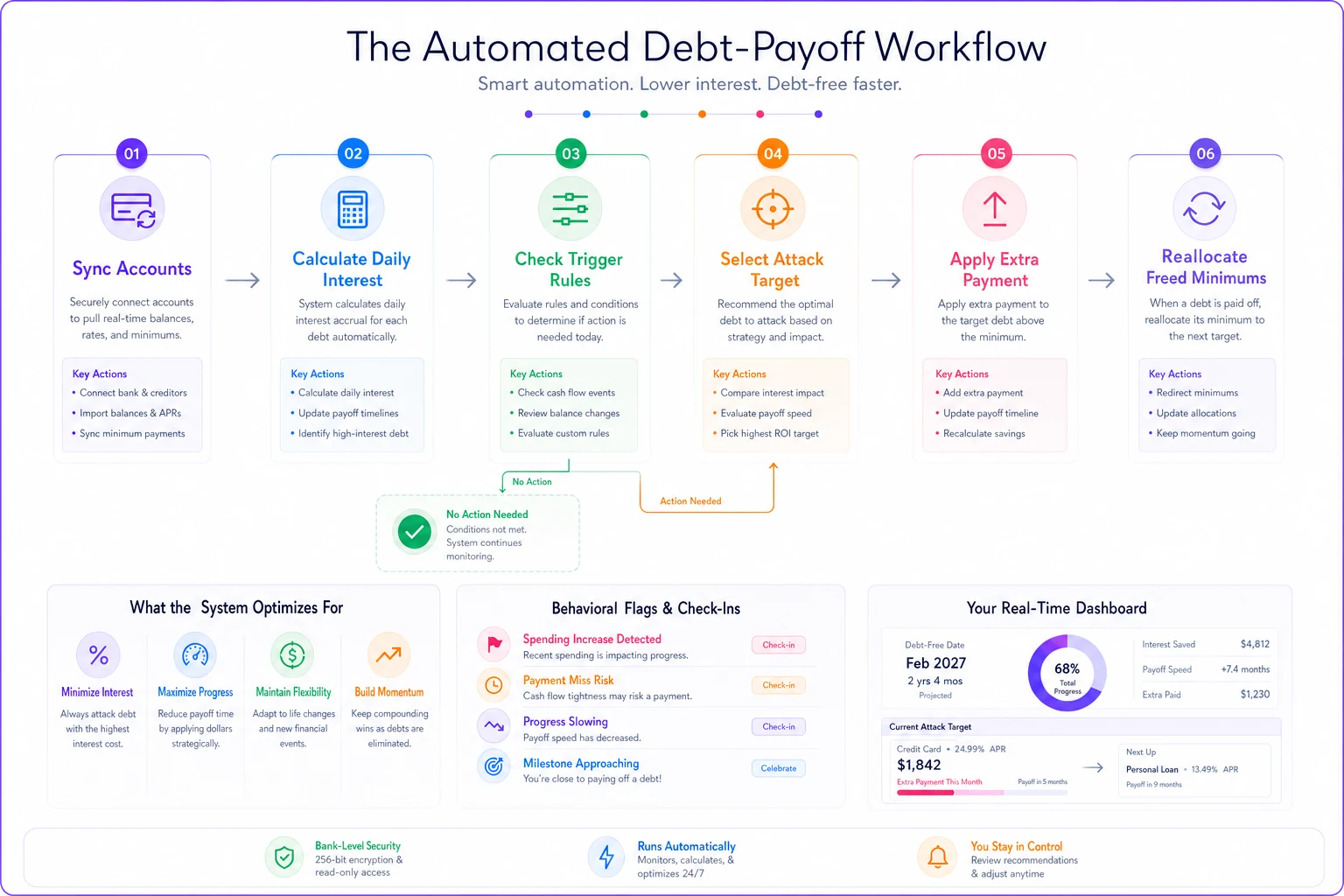

Software automation that removes friction

Manual tracking kills consistency. Most people try spreadsheets and abandon them within a few weeks — not because they're lazy, but because recalculating allocations every month while life is happening is genuinely tedious.

AI-powered operational software can handle the math side of this. Platforms built around personal finance workflows can monitor balances, calculate daily interest accrual, and flag when you're approaching a trigger point — sending you something like "you can eliminate your store card this month by adding $127 to your payment" instead of making you figure that out yourself.

The automation handles calculations while you focus on execution. It can also track behavioral patterns — missed payments, growing balances — and surface the right strategy adjustment at the right time. More practically, it redirects freed minimums automatically rather than letting lifestyle creep absorb them.

A basic automated workflow looks something like this:

-

Balances and minimums sync from connected accounts each month

-

System calculates daily interest accrual per debt

-

Trigger rules are checked against current balances and payment history

-

Recommended attack target and extra payment amount are surfaced

-

Freed minimums from cleared debts are automatically reallocated to the next target

-

Behavioral flags (missed payments, avoidance patterns) prompt a strategy check-in

Here's a simple visual of that automation workflow.

Not glamorous, but removing those manual steps is what keeps the plan alive past month three.

Common execution failures

The biggest failure is perfectionism paralysis. People spend weeks optimizing their strategy, building elaborate spreadsheets, researching rate differences. Meanwhile they're making minimums and accruing interest. A decent plan executed today beats a perfect plan that starts next month.

The second failure is social pressure. Your coworker swears by avalanche. Your brother cleared his debt with snowball. You switch based on whoever you talked to last. Your trigger rules are your trigger rules — don't negotiate them based on someone else's situation.

The third failure is lifestyle creep mid-progress. Clear two credit cards and suddenly the freed $200 starts going to restaurants instead of debt acceleration. Automating transfers that immediately redirect freed minimums removes this temptation from the equation entirely.

Your first 90 days

Week one: List everything. Every debt, rate, balance, minimum payment. No optimization yet.

Week two: Calculate your pure avalanche order and pure snowball order. Note where they differ.

Week three: Apply the hybrid rules. Mark debts over 20% for immediate avalanche. Flag sub-$1,000 debts for quick wins. Sort the rest by your current motivation level.

Month two: Execute your first target relentlessly. No strategy switching for 60 days minimum. Track every payment.

Month three: Assess. Did you hit your target? Are you maintaining momentum? Hit any trigger points? Adjust if needed, then commit to another 60 days before the next assessment.

The reality of extended timelines

Most debt payoffs take 18–36 months, not the six months you see in success stories. This is why psychological sustainability matters more than mathematical optimization. You're not sprinting; you're running a marathon with strategic sprint intervals built in.

Around months 7–12, most people hit a wall. Initial wins are behind you, big debts still loom, and life keeps happening. This is when your trigger rules do the work. Instead of abandoning the plan, you pivot temporarily, clear one small win, then return to the main track.

Months 13–18 bring a different problem: acceleration anxiety. The finish line is visible and people try to sprint too hard. Unsustainable budget cuts, relationship stress, burnout right before the end. The hybrid system forces measured progress — staying with what actually got you this far rather than blowing up the plan in the final stretch.

Making peace with imperfect progress

A hybrid debt payoff system is built around human reality. You'll have bad months where you only make minimums. You'll have windfalls where you clear multiple debts at once. You'll adjust based on life, and that's fine.

The goal isn't perfect execution — it's consistent progress. Clear trigger rules remove daily decision fatigue while maintaining flexibility for real circumstances. You get the mathematical benefits of avalanche when you're strong and the psychological benefits of snowball when you're not.

Stop arguing about which method is better. Build a system that uses both, automate what you can, and focus on moving forward. Your future self won't care whether you followed pure avalanche or pure snowball. They'll care that the debt is gone.

Ready to master your money?

Join thousands of users leveraging Savioly to build smarter budgets, save more efficiently, and plan for a secure financial future.