Most expense tracking fails because people categorize spending the way accounting software tells them to. "Dining out" goes here, "groceries" go there, "entertainment" gets its own bucket. Then what? You look at the numbers each month, feel vaguely guilty about restaurant spending, promise to do better, and nothing changes.

The real problem isn't tracking accuracy. It's that traditional expense categories don't connect to actual decisions. When you see "$847 on dining out," what are you supposed to do with that? Cut it in half? Stop eating out entirely? Only go on weekdays?

Small business owners who actually changed their spending habits did something different. They organized expenses around decision points, not accounting categories.

Why your current categories aren't helping

Why your current expense categories aren't helping you spend differently

Most expense tracking fails because people categorize spending the way accounting software tells them to. "Dining out" goes here, "groceries" go there, "entertainment" gets its own bucket. Then what? You look at the numbers each month, feel vaguely guilty about restaurant spending, promise to do better, and nothing changes.

Analysis paralysis from traditional categories

Why traditional categories create analysis paralysis

Take charge of your finances with clarity and confidence.

Savioly gives you real-time visibility and actionable steps to improve your money management.

- Automated expense tracking

- Goal-based saving plans

- Personalized financial insights

No credit card required

Standard expense categories feel logical until you try using them to change behavior. A category like "Transportation" might include your car payment, insurance, gas, maintenance, Uber rides, and that random bike rental from vacation. Some of those are fixed costs you can't touch. Others are daily decisions. Lumping them together makes the whole category feel untouchable.

Same thing with "Utilities." Your electricity bill sits next to your Netflix subscription and internet service. One fluctuates based on usage you could realistically change. The others are basically fixed until you actively cancel or renegotiate. Grouped together, the whole thing becomes background noise.

Even worse, traditional categories completely miss the emotional triggers behind spending. That coffee shop visit might technically be "dining," but functionally it's your mobile office. The gym membership filed under "Health & Fitness" might actually be about social connection. When categories ignore the why behind spending, they can't help you make better decisions.

Decision-aligned categories

Decision-aligned categories that drive action

A decision-focused system groups spending by three things: how much control you have, how often you make the choice, and what triggers the expense. This creates categories that suggest actions rather than just displaying numbers.

Locked Costs are true fixed expenses you've already committed to — rent, insurance premiums, loan payments, contracted services. These require formal action to change. You review these quarterly, not monthly.

Habit Spending covers regular purchases you make without thinking: morning coffee, lunch at work, weekly grocery runs, Friday takeout. These respond to routine changes and environmental design. Block the food delivery apps. Pack lunch on Sundays. Switch coffee shop routes.

Impulse Zones capture spontaneous spending triggered by situations: stressed shopping, boredom purchases, social pressure, convenience premiums. These need specific interventions at the point of decision — add friction, create waiting periods, set up obstacles.

Investment Purchases include spending meant to save money or time later: bulk buying, tools, courses, equipment upgrades. These need better evaluation frameworks, not elimination. Calculate actual payback periods. Track whether previous investments actually delivered.

Joy Spending covers purchases that genuinely improve life quality when done intentionally — hobbies, experiences, gifts, celebrations. These shouldn't be cut. They should be protected and planned. The goal is increasing the joy-per-dollar ratio, not eliminating the category.

Here's a quick comparison of how these categories differ from standard accounting buckets:

| Traditional Category | Decision-Aligned Category | What It Tells You |

|---|---|---|

| Dining Out | Avoiding Cooking / Workday Convenience Food | The trigger, not just the merchant |

| Transportation | Locked Costs vs. Daily Choices | What's actually changeable |

| Utilities | Fixed Subscriptions vs. Usage-Based | Where action is even possible |

| Shopping | Impulse Zone / Keeping Up Appearances | The emotional driver |

| Health & Fitness | Investment Purchase / Social Connection | The real function |

Here's a quick comparison of how these categories differ from standard accounting buckets:

Naming rules for your taxonomy

Building your personal taxonomy with naming rules

Generic category names get generic results. "Eating Out" doesn't tell you anything actionable. But "Workday Convenience Food" or "Lazy Evening Delivery" immediately reveals the decision point.

Start with your last three months of transactions. Instead of sorting by merchant type, sort by situation. What triggered each purchase? Were you solving a problem? Responding to an emotion? Following a routine?

Name categories based on the decision moment, not the expense type:

-

"Didn't Plan Ahead" instead of "Convenience Store"

-

"Avoiding Cooking" rather than "Restaurant"

-

"Bored at Home" not "Entertainment"

-

"Keeping Up Appearances" instead of "Clothing"

These names might feel a little harsh. That's partly the point. Every time you categorize an expense, you're confronting the actual decision you made. This creates natural friction that changes behavior before the next purchase, not just guilt after reviewing last month's damage.

Some purchases legitimately fit multiple categories. A business dinner might be "Client Relationship" (investment) or "Networking Pressure" (impulse) or "Legitimate Celebration" (joy). The act of choosing forces you to examine your real motivations.

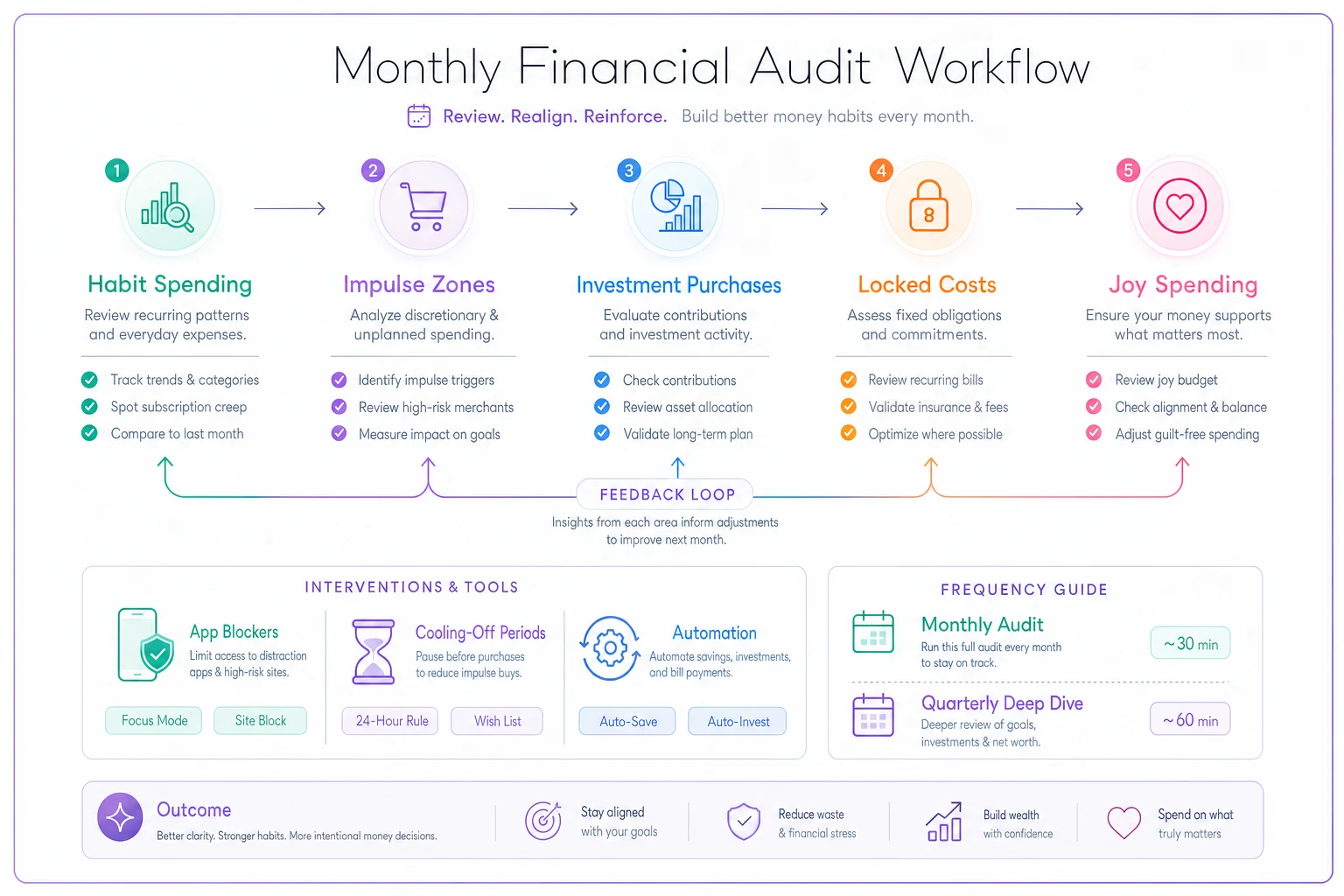

Monthly audit process

The monthly audit that creates compound behavior change

Traditional expense reviews focus on totals and trends. Did I spend more or less than last month? Am I over budget? These questions lead to vague resolutions about "spending less" without addressing specific decision patterns.

A behavior-focused audit examines decision quality, not just quantities. Each month, you're looking for three things: patterns that surprised you, categories that grew unexpectedly, and interventions that actually worked.

How to run the audit — in order:

-

Start with Habit Spending. These purchases happen automatically, so small changes compound fast. If "Morning Coffee Shop" totaled $127 last month, the question isn't whether that's too much. It's whether you're getting $127 of value — productivity, social connection, routine stability — from that habit. Maybe you are. Maybe the coffee shop is genuinely where you do your best thinking. Then it's not an expense to cut but an investment to optimize. Buy the monthly plan. Negotiate a regular's discount.

-

Move to Impulse Zones. Look for timing patterns. Do most impulse purchases happen on specific days? After certain events? During particular emotional states? One person discovered nearly 70% of their "Stressed Shopping" happened between 8–10pm on weekdays. They set up automatic app blockers during those hours. Spending dropped noticeably without feeling like deprivation.

-

Pull every Investment Purchase from the past six months. How many actually delivered? That $200 course — did you finish it? The bulk paper towels — did you actually save money or just use more? Track investment success rates like a portfolio. If fewer than half deliver, you need better evaluation criteria before the next one.

-

Review Locked Costs quarterly, not monthly. These rarely change and don't need monthly attention. Flag anything with an upcoming renewal or contract end date.

-

End with Joy Spending. Don't cut this category. Ask whether the money went toward things that actually felt good or just things that seemed like they should. Protect the ones that genuinely delivered.

This diagram shows the audit flow and where to apply interventions.

The whole process shouldn't take more than 30 minutes if your categories are set up correctly.

Intervention rules that stick

Creating intervention rules that stick

Rules without enforcement mechanisms are just wishes. Most people create spending rules that require constant willpower: "I won't eat out this month" or "No more online shopping." These fail because they fight against existing patterns instead of redirecting them.

Effective interventions add friction to unwanted behaviors and remove friction from desired ones. They work with your psychology, not against it. Instead of "no restaurant spending," try "restaurant spending requires walking there." Instead of "no online shopping," implement a 48-hour waiting period before purchasing.

For Habit Spending:

-

Automate the positive habits (subscriptions for things you'd buy anyway)

-

Add steps to negative habits (unlink payment methods, delete apps)

-

Replace expensive habits with cheaper alternatives that serve the same purpose

-

Bundle habits together (coffee shop only when bringing lunch from home)

For Impulse Zones:

-

Create cooling-off periods (save items to lists, revisit after waiting)

-

Set up approval requirements (text purchases to an accountability partner)

-

Limit payment methods (cash only for problem categories)

-

Schedule "impulse windows" (Sunday afternoon shopping hour)

For Investment Purchases:

-

Require a basic business case before buying

-

Set payback period requirements (must return value within 3 months)

-

Track previous investment performance

-

Create "earned investment" rules (new investment only after last one pays off)

Make the intervention automatic, not voluntary.

The key is making the intervention automatic, not voluntary. Apps that block purchases, payment methods that require extra steps, accountability systems that trigger without your input — these create lasting change. Willpower-based rules create temporary guilt.

Software automation for tracking

Software automation for expense tracking

Manual categorization kills momentum. By the time you sit down to categorize last month's expenses, the decisions are ancient history. The behavioral moment passed weeks ago. This is where properly configured expense tracking software becomes essential — not for pretty charts, but for real-time decision intervention.

Modern expense categorization platforms can auto-classify transactions based on your custom rules, flag patterns as they develop, and send alerts before problems compound. When "Stressed Shopping" hits $50 in a week, you get notified before it becomes a $300 month. When "Investment Purchases" exceed their success rate threshold, the system prompts evaluation before the next one goes through.

The automation handles tedious tracking so you can focus on decisions. Instead of spending an hour categorizing transactions, you spend five minutes reviewing patterns and adjusting interventions. The system remembers your rules, applies them consistently, and surfaces only the insights that actually demand attention.

Some platforms include behavioral triggers — blocking certain purchase categories during predetermined times, requiring confirmation before specific expenses, or automatically moving money to savings when problem categories stay under target. These features shift expense tracking from historical record-keeping into active behavior modification.

Evolving your categories

When categories need evolution

Categories that worked six months ago might be irrelevant now. Life changes, priorities shift, and yesterday's problem becomes a non-issue. A category system that doesn't evolve becomes another abandoned spreadsheet.

Review your taxonomy quarterly. Which categories consistently have zero entries? Those can go. Which have become too broad? Split them. Which interventions stopped working? Replace them.

Pay attention to uncategorized expenses. If the same type of transaction keeps landing in "Other," you've found a blindspot — maybe a new habit forming, maybe an old pattern you've been avoiding. Either way, it needs its own category and intervention rule.

Sometimes entire category groups need restructuring. That detailed breakdown of seventeen different food categories might have been useful when you were learning to cook. Now that meal prep is automatic, you might only need "Planned Meals" and "Deviation Meals." Simplification often signals progress.

Sustainability over perfection

Making the system sustainable

The perfect categorization system that you abandon after two months is worse than a basic system you maintain for years. Sustainability beats sophistication.

Start with five to seven categories. Make them obvious enough that categorization takes seconds, not minutes. If you're debating where something belongs for more than ten seconds, your categories are too complex.

Choose intervention rules you can actually implement. "Check bank balance before every purchase" sounds responsible but isn't realistic for most people. "Check category spending every Sunday" actually happens. Work with your actual behavior patterns, not your idealized ones.

Build review rhythms that match your life. If monthly reviews are too frequent, do quarterly. If you're detail-obsessed, do weekly. The schedule matters less than consistency. Three quarterly reviews beat twelve planned monthly reviews where only two actually happen.

Most importantly, measure success by behavior change, not tracking perfection. Missing a few categorizations doesn't matter if your problem spending drops significantly. Having gorgeous reports means nothing if your habits never change.

Applying the approach beyond finance

Beyond personal finance

The same decision-focused approach that changes personal spending can transform business expenses, time management, even how you allocate energy in relationships. The principle holds: organize around decision points, not traditional categories.

A business might categorize expenses as "Growth Investments," "Maintenance Costs," "Panic Purchases," and "Strategic Bets" instead of standard accounting buckets. A time audit might use "Deep Work," "Reactive Tasks," "Relationship Building," and "Recovery" instead of project codes.

The power isn't in the specific categories — it's in the connection between classification and action. When every category maps to a clear decision or intervention, tracking becomes transformation. The monthly audit becomes a strategic review. The expense report becomes a behavior change tool.

Stop categorizing expenses to satisfy accounting software or match what financial blogs recommend. Build categories that reflect your actual decision points, name them honestly, and create interventions that work automatically. The right taxonomy doesn't just track spending — it actively changes it.

Stop categorizing expenses to satisfy accounting software or match what financial blogs recommend. Build categories that reflect your actual decision points, name them honestly, and create interventions that work automatically. The right taxonomy doesn't just track spending — it actively changes it.

Ready to master your money?

Join thousands of users leveraging Savioly to build smarter budgets, save more efficiently, and plan for a secure financial future.