This runway budgeting system came out of necessity when I started freelancing. Traditional budgets assume steady paychecks—mine came in chunks of $8,400 one month, then $1,200 the next, then $11,000 two months later. Standard budget templates broke immediately. After burning through savings twice and nearly missing rent, I built this approach. It treats your finances the way a business treats cash flow—not as money you have, but as time you've bought. The system now runs automatically across three checking accounts and takes maybe 20 minutes a month to maintain.

Why traditional budgeting fails with irregular income

Budget apps assume predictable income. They divide your annual income by twelve, allocate percentages to categories, and then wonder why freelancers constantly overspend or underspend.

The core problem: traditional budgets match spending to income timing. When a $15,000 project payment hits, the budget says you have $15,000 to allocate this month. Human psychology immediately inflates lifestyle to match. Then three lean months arrive and everything collapses.

Irregular earners face three interlocking problems. Income clustering creates false abundance—that $15,000 feels permanent even though it needs to last four months. Expense timing never aligns with income timing. Rent hits monthly whether you've been paid or not. And decision fatigue multiplies when every purchase requires mentally calculating remaining runway.

Traditional percentage-based budgeting makes this worse. Saving "20% of income" means nothing when income swings 400% month to month. Fixed expense budgets assume you know next month's income. Zero-based budgets reset constantly, destroying any spending rhythm.

The runway calculation that changes everything

Runway budgeting flips the model. Instead of matching spending to income, you match spending to time. The core metric becomes months of expenses covered, not dollars in accounts.

Take charge of your finances with clarity and confidence.

Savioly gives you real-time visibility and actionable steps to improve your money management.

- Automated expense tracking

- Goal-based saving plans

- Personalized financial insights

No credit card required

Start by calculating your true monthly run-rate. This isn't an average—averages lie when income varies wildly. Pull twelve months of bank statements and build three numbers:

Survival run-rate: The absolute minimum to keep functioning. Rent, insurance, minimum food, critical bills. No entertainment, no savings, no extras. Most people land somewhere between $2,800 and $4,200 monthly.

Baseline run-rate: Normal life without stress. All bills, reasonable food budget, some entertainment, small savings contribution. Usually 40-60% above survival. If survival is $3,200, baseline probably runs $4,500–$5,100.

Comfortable run-rate: Life with actual breathing room. Full savings, occasional restaurants, hobby spending, small splurges. Generally 25-35% above baseline.

These aren't aspirational numbers. Calculate from actual spending history, then reduce by 10-15% to build buffer. The goal isn't perfection—it's sustainability.

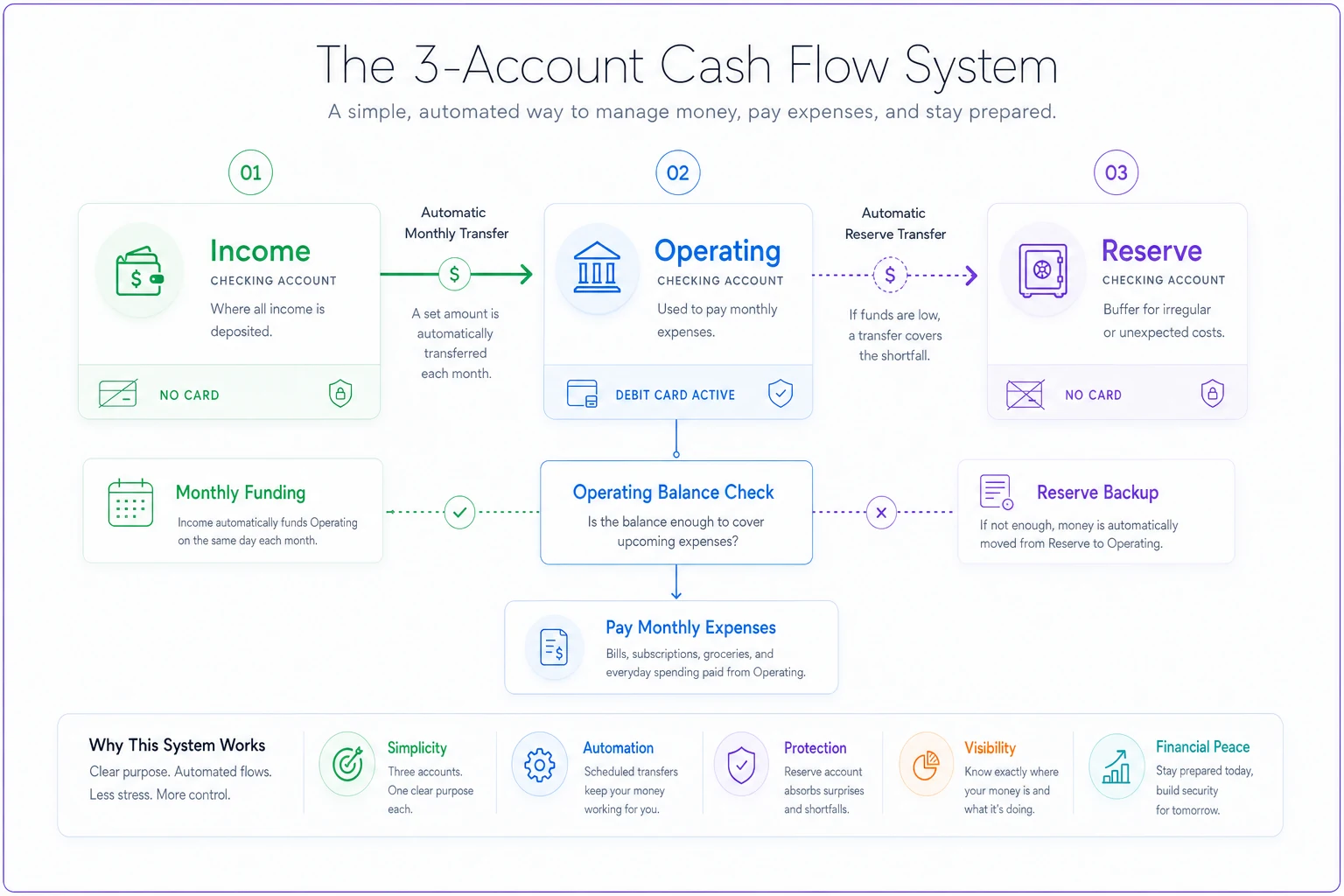

Setting up the three-account runway system

Physical separation beats mental math every time. The system uses three checking accounts at the same bank to create discipline without requiring constant willpower.

Income account: All money enters here first. Client payments, tax refunds, side gigs, everything. This account has no debit card, no checks, no spending access. It's purely a reservoir.

Operating account: Your monthly run-rate transfers here automatically. This account has your debit card and pays all bills. When it's empty, spending stops until next month's transfer.

Reserve account: Emergency buffer holding 3-6 months of survival run-rate. No card access. Only touched during genuine emergencies or to cover operating shortfalls.

The transfer schedule is where the magic actually happens. Every month on the 1st, your baseline run-rate moves from Income to Operating. If Income can't cover it, Reserve makes up the difference. Operating never holds more than one month of spending.

This diagram shows the monthly flow between Income, Operating, and Reserve.

This separation eliminates overspending temptation. When Operating runs low, you naturally reduce spending instead of dipping into next month's money. The Income account balance divided by monthly run-rate shows exact runway remaining—no complex calculations needed.

Calculating sustainable run-rate from volatile income

Finding the right run-rate takes roughly three months of data analysis. Don't use simple averages—they'll burn you during lean periods.

Map income patterns first. Some freelancers see quarterly clustering ($2k, $2k, $18k, repeat). Others face pure randomness. Commission workers might see seasonal patterns. Plot eighteen months to spot cycles.

Calculate your sustainable run-rate using the 70% rule. Take your worst six-month period from the past eighteen months. Calculate average monthly income during that stretch. Multiply by 0.7. That's your maximum sustainable run-rate.

Example: Worst six months averaged $5,800 monthly. Multiply by 0.7 = $4,060 maximum sustainable run-rate. Even if good months average $12,000, spending stays at $4,060. The excess builds runway for lean periods.

Adjust quarterly based on runway depth:

-

Under 3 months runway

Drop to survival run-rate immediately

-

3-6 months runway

Use 70% calculation

-

6-9 months runway

Can push to 80% calculation

-

Over 9 months runway

Safe at 85% calculation

The system self-corrects. Overspending shrinks runway, forcing a lower run-rate. Good months extend runway, allowing gradual increases. No guessing required.

Allocation buckets that match irregular income reality

Within your Operating account, create mental or sub-account buckets. Unlike traditional categories, these buckets recognize that income is irregular.

-

Fixed bucket (40-50% of run-rate)

Rent, insurance, subscriptions, loans. These hit regardless of income. Automate everything possible.

-

Flexible bucket (25-30% of run-rate)

Food, transport, utilities. These vary but stay within ranges. Track weekly to adjust spending pace.

-

Discretionary bucket (15-20% of run-rate)

Entertainment, hobbies, clothing. First to cut during lean months.

-

Buffer bucket (10-15% of run-rate)

Stays in Operating. Covers small overages and timing gaps. Never fully depleted.

Automate the Fixed bucket transfers first so essential bills are never at risk when income spikes or drops.

Critical difference from normal budgeting: buckets are guidelines, not rules. When income is strong and runway extends past nine months, buckets can flex up 20%. When runway shrinks below four months, they contract 30%. The system breathes with your income instead of forcing rigid categories.

Transfer schedules based on income patterns

Payment frequency determines optimal transfer timing. Monthly transfers work for most, but specific patterns need adjustment.

Quarterly cluster pattern (common in consulting): Income arrives in chunks every 3-4 months. Set weekly transfers at run-rate divided by 4.3. Smaller, frequent transfers prevent overspending after big payments hit.

Random pattern (typical freelancing): No predictable timing. Use bi-weekly transfers at run-rate divided by 2. More frequent movement maintains spending awareness without constant management.

Seasonal pattern (retail commission): Predictable strong and weak periods. During strong months, transfer at 60% of normal run-rate and bank the excess. During weak months, transfer at 120% from reserves.

Project-based pattern (contract work): Large payments with gaps. Transfer daily at run-rate divided by 30. Sounds extreme but prevents lifestyle inflation after big deposits.

Automation is mandatory. Manual transfers fail within three months—reliably. Set up automatic recurring transfers based on your pattern. Adjust amounts quarterly, not monthly. Frequent tweaking destroys the system's stability.

The transfer schedule creates artificial scarcity that matches spending to sustainable levels. Even with $50,000 sitting in the Income account, Operating stays limited to sustainable run-rate. Psychology adjusts to Operating balance, not total wealth.

The 90-day runway monitoring routine

Runway depth determines every financial decision. Track it monthly with this routine.

Every month on the 25th—before month-end chaos—calculate:

-

Total runway funds = Income account + Reserve account + remaining Operating balance

-

Monthly run-rate (current level)

-

Runway months = Total funds ÷ Monthly run-rate

Based on runway depth, adjust next month:

| Runway Months | Action Required | Run-Rate Adjustment |

|---|---|---|

| Under 2 | Emergency mode | Drop to 75% of survival rate |

| 2-3 | Caution zone | Use survival run-rate |

| 3-5 | Stable zone | Use 70% calculation baseline |

| 5-8 | Growth zone | Can increase to 80% calculation |

| 8-12 | Comfort zone | Safe at 85% calculation |

| Over 12 | Investment zone | Maintain 85%, invest excess |

Track three metrics monthly:

-

Runway depth (primary metric)

-

Burn rate vs. income rate (trending up or down)

-

Bucket adherence (which buckets consistently overrun)

When runway drops two months consecutively, cut run-rate immediately. Don't wait for the third month. When runway grows three consecutive months, consider raising run-rate next quarter.

The monitoring routine takes around 20 minutes monthly but prevents every financial crisis. You'll spot problems 2-3 months before they hit, giving time to adjust spending or push harder on income.

Common failure points and fixes

Failure 1: Treating windfalls as bonuses When unexpected money arrives—tax refund, bonus project, gift—the temptation is to spend outside the system. All money goes through Income account, no exceptions. Celebrate windfalls by watching runway extend, not by spending them.

Failure 2: Borrowing from future months Operating is empty but Income has money. "Just this once" transfers destroy the system. When Operating empties, spending stops. The constraint is the system working.

Failure 3: Not adjusting for life changes Moving, relationship changes, job shifts all affect run-rate. Recalculate after major changes. The system assumes relatively stable circumstances. When those change, the numbers must change too.

Failure 4: Hiding expenses from the system Credit cards, payment plans, informal borrowing—all let you spend outside Operating. This creates invisible burn rate. All spending must flow through Operating for the system to function.

Failure 5: Perfectionism paralysis Trying to nail exact run-rate calculations, perfect bucket percentages, optimal transfer timing. Start with rough numbers and adjust quarterly. Perfect is the enemy of sustainable.

Making the system bulletproof with templates

A simple spreadsheet beats complex apps for runway budgeting. Here's the essential structure:

Income Tracker Tab

-

Date received

-

Amount

-

Source

-

Running total for month

-

6-month rolling average

-

12-month rolling average

Runway Calculator Tab

-

Current Income account balance

-

Current Reserve account balance

-

Current Operating account balance

-

Total available funds

-

Current monthly run-rate

-

Calculated runway months

-

Historical runway (graph last 12 months)

Monthly Review Tab

-

Actual spending vs. run-rate

-

Bucket performance

-

Runway change from last month

-

Income vs. burn rate trend

-

Adjustment recommendations

Scenario Planner Tab

-

What-if calculations

-

If income stops today, how long until each threshold

-

If income doubles, when to raise run-rate

-

Break-even points for different run-rates

Keep it simple. Fancy features create maintenance burden. The spreadsheet should take five minutes to update monthly, not thirty.

When to break the rules

Sometimes the system needs an override. Knowing when prevents rigid thinking from creating worse problems.

Break rules when:

-

One-time medical expenses exceed Buffer bucket

-

Critical income-generating equipment fails

-

A genuine opportunity requires investment with a clear ROI

-

Runway exceeds 12 months consistently for 6+ months

Never break rules for:

-

Lifestyle inflation temptations

-

Social pressure spending

-

"Investment" opportunities without clear return

-

Emotional or impulse purchases

-

Holiday or vacation spending beyond buckets

Rule breaks should be rare—maybe two or three times a year—documented, and corrected within 60 days. If you're breaking rules monthly, the run-rate is too low or spending habits need work.

The psychological shift that makes it sustainable

Runway budgeting reframes money from "what I have" to "time I've bought." That shift changes more than you'd expect.

Instead of seeing $20,000 and feeling rich, you see 5.2 months of runway and feel secure but motivated. Instead of panicking over a slow month, you watch runway drop from 5.2 to 4.8 months and adjust calmly.

The system removes daily money stress by answering one question: "How long can I maintain this?" When that answer stays above three months, anxiety mostly disappears. When it drops below three months, clear actions exist.

Traditional budgeting for irregular income creates constant self-negotiation. Every purchase becomes a complex calculation of future income probability. Runway budgeting eliminates the negotiation—Operating account balance makes decisions binary. Money exists or it doesn't.

Adjustments for different income types

Each income type has different volatility patterns. The core system stays the same, but parameters adjust. Don't copy someone else's numbers—calculate based on your specific pattern.

-

Freelancers and consultants

Start conservative with 60% of average income as run-rate. These incomes are most volatile. Build to 9-month runway before raising run-rate.

-

Commission-based sales

Use 70% of worst quarter as baseline. Sales incomes cluster around performance periods. Keep 6-month runway minimum to weather slow seasons.

-

Gig economy workers

Calculate weekly instead of monthly. Income varies too frequently for monthly calculations. Daily transfers help maintain awareness.

-

Seasonal workers

Split the year into seasons. High season run-rate can be 50% higher than low season. Transfer excess from high to low season automatically.

-

Mixed income (part-time + freelance)

Treat steady income as baseline, irregular income as runway builder. Set run-rate at steady income plus 30% of average irregular income.

Each income type has different volatility patterns. The core system stays the same, but parameters adjust. Don't copy someone else's numbers—calculate based on your specific pattern.

Building your runway system this week

Implementation takes one weekend and three checking accounts. Start with rough numbers and refine later.

-

Day 1

Open accounts, calculate run-rates from bank history

-

Day 2

Set up automatic transfers, fund initial amounts

-

Day 3

Create tracking spreadsheet, run first scenario tests

-

Week 1

Live normally but track everything through Operating account

-

Month 1

First full month on system—expect roughly 20% overage

-

Month 2

Adjust run-rate based on Month 1 reality

-

Month 3

System stabilizes and becomes automatic

The hardest part is starting before you feel ready. The system teaches through operation, not planning. Your first run-rate will be wrong. Buckets will need adjustment. Transfer schedule will need tweaking. That's all normal.

A rough system running beats a perfect system planned. Start with any number close to reasonable and adjust as you learn your real patterns.

Conclusion

Budgeting irregular income doesn't require complex math or perfect prediction. It requires accepting that income varies but expenses don't, then building a system that creates artificial stability.

The runway system works because it matches human psychology. We naturally spend what's available in our checking account. By controlling what's available through automatic transfers, we control spending without constant willpower.

After running this system for five years, my income still varies wildly—last year it ranged from $1,800 to $19,000 monthly. But lifestyle stays consistent, stress stays manageable, and runway stays above six months. The system handles the variation so I don't have to.

Traditional budgets pretend irregular income is regular. That's why they fail. Runway budgeting accepts irregularity and builds stability anyway. It's not about predicting the future or controlling income—it's about creating a sustainable present regardless of what comes next.

Start this week. Open the accounts, calculate a rough run-rate, set up transfers. In three months, you'll wonder how you managed the chaos without it.

Ready to master your money?

Join thousands of users leveraging Savioly to build smarter budgets, save more efficiently, and plan for a secure financial future.