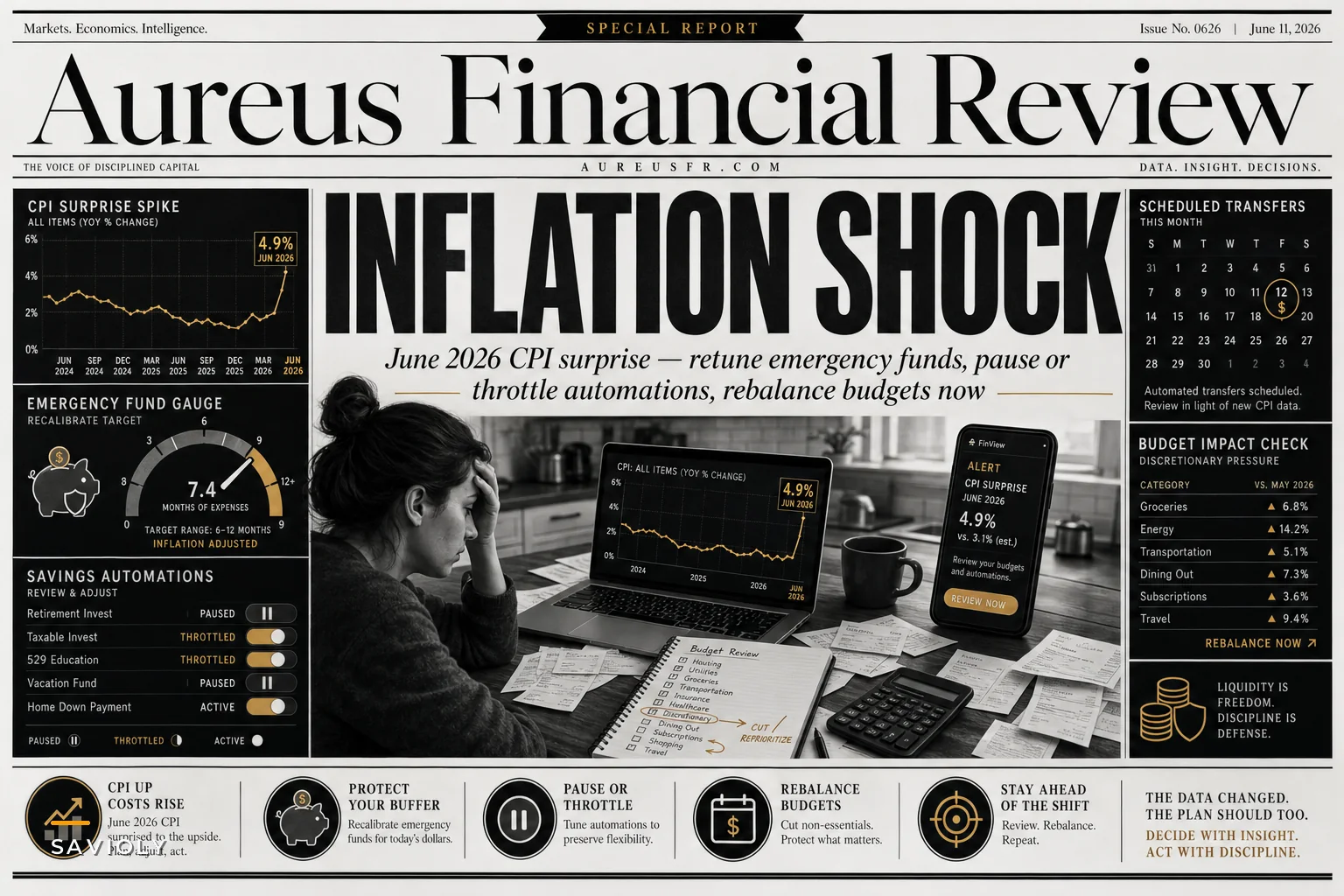

The June 2026 CPI numbers just dropped, and they're not what anyone wanted to see. The Bureau of Labor Statistics report shows inflation running hotter than expected—again. If you've been coasting on the same automated savings percentages and budget allocations from six months ago, you're probably feeling the squeeze right about now.

This isn't about whether the Fed will pivot or hold. That's noise. What matters is that your grocery bill jumped another 4.2% quarter-over-quarter, your landlord's already hinting at renewal terms, and those automated transfers to your vacation fund are starting to hurt when you need cash for actual expenses.

Most people set up their savings automations during calmer periods and then forget about them. Your 401k contribution, your emergency fund transfer, that $300 monthly sweep into your house downpayment account—they all made sense when you configured them. But persistent inflation creates a compounding problem: expenses creep up while automated savings stay rigid, slowly strangling your monthly cash flow until something breaks.

The emergency fund paradox nobody talks about

Standard emergency fund advice during inflationary periods is kind of broken. Everyone says maintain 3-6 months of expenses. Fine. But which expenses? Last year's? This year's projected? Next year's estimated?

Someone I know calculated their emergency fund needs based on 2025 spending. Their actual June 2026 expenses were running 18% higher. That's not lifestyle creep—that's pure inflation across housing, food, transportation, and healthcare. Their "6-month cushion" was actually closer to 5.1 months. By December, it'll probably be 4.8 if trends hold.

The math gets worse when you factor in opportunity cost. That $24,000 emergency fund sitting in a "high-yield" savings account at 4.5% is losing purchasing power when inflation's running at 5.8%. You're literally paying to stay liquid.

Most financial planning software treats emergency funds as static targets. Hit $20k, check the box, move on. But inflation turns that static target into a treadmill. You need dynamic sizing that adjusts quarterly, not once a year.

Start here: take your last three months of actual spending—not budgeted, actual. Add 8% for forward inflation coverage. That's your new monthly burn rate for emergency fund calculations. If you were targeting six months of coverage, you need to true-up based on this inflated number.

Recalculate your emergency target quarterly instead of annually to keep pace with persistent inflation.

Yes, it's painful to move your emergency fund target from $18,000 to $21,000 when cash flow is already tight. But it's more painful to discover your safety net has a hole in it when you actually need it.

Why your automated savings percentages are lying to you

Percentage-based automation seemed smart when you set it up. 15% to retirement, 10% to short-term savings, 5% to vacation fund. Clean, simple, hands-off.

Take charge of your finances with clarity and confidence.

Savioly gives you real-time visibility and actionable steps to improve your money management.

- Automated expense tracking

- Goal-based saving plans

- Personalized financial insights

No credit card required

Except percentages assume your income and expenses scale together. They don't. Not during inflationary shocks.

Your salary might have gone up 3% this year if you're lucky. Your landlord just announced a 7% increase. Groceries are up 12% despite buying less. Those fixed percentage automations are now routing money you need for necessities toward goals that suddenly feel a lot less urgent.

"Pay yourself first" is solid advice in normal conditions. But when paying yourself first means choosing between your Roth IRA and fixing your car's transmission, the automation has failed its purpose.

Here's the adjustment framework that actually works:

First, figure out your true discretionary income after inflation-adjusted essentials. Not what you budgeted—what you're actually spending on housing, food, transportation, insurance, and utilities over the last 60 days. That's your real baseline.

Take whatever's left and apply a 40/40/20 split temporarily:

-

40% maintains current automated savings (reduced from your previous percentage)

-

40% goes to a tactical reserve fund (different from your emergency fund—more on that below)

-

20% stays liquid for inflation volatility

This probably means cutting your 401k contribution from 15% to around 9% temporarily. If dropping below the employer match threshold, you're leaving money on the table—but if the alternative is credit card debt at 24% APR to cover an expense spike, the math still supports the adjustment.

The tactical reserve fund—your new inflation buffer

You need a third bucket beyond checking and emergency savings during volatile inflation. Call it a tactical reserve, opportunity fund, whatever you want.

This isn't emergency money. Your car breaking down is an emergency. Your grocery bill running $80 over every single week isn't—it's the new normal your budget hasn't caught up to yet.

Size this fund at 1.5 months of the gap between your pre-inflation budget and current reality. If monthly expenses went from $4,500 to $5,100, you need $900 in tactical reserves ($600 gap × 1.5 months). This money handles the constant small overages while you restructure your core budget.

Resequencing your financial priorities (temporarily)

Personal finance orthodoxy has a sacred order: emergency fund, high-interest debt, retirement, everything else. That sequence assumes stable conditions. June's CPI data is a pretty clear signal we're not there.

Your temporary resequencing should look like this:

Immediate priorities (next 90 days):

-

One month of inflated expenses in checking (liquidity buffer)

-

Tactical reserve fund (1.5 months of inflation gap)

-

Minimum payments on everything

-

Emergency fund true-up to inflated expenses

Secondary priorities (months 4-6):

-

High-interest debt minimums plus tactical payments

-

Retirement contributions at employer match threshold only

-

Pause all other automated savings

Restoration triggers (when to reverse course):

-

Three consecutive months where actual expenses match or fall below budget

-

Income increase that exceeds inflation by 2%+

-

Tactical reserve untouched for 60 days

This feels like retreating. It's not. You're trading long-term optimization for short-term stability, which is exactly what an inflationary shock calls for.

The savings automation audit you need to run today

Pull up your bank's scheduled transfers right now. Every automated transfer needs to answer three questions:

-

Can I reduce this by 30% without triggering penalties or losing benefits?

-

If I paused this for 90 days, what would break?

-

Is this transfer funding a goal that still makes sense given 5.8% inflation?

Most people find they're funding goals on autopilot that no longer align with reality. That European vacation fund sweeping every month? Maybe that becomes a tactical reserve. The new car fund? Your current car just got a 12-month life extension.

For each automation that survives the audit, add a review trigger. Not a calendar reminder you'll ignore—an actual trigger based on your checking account balance. If checking drops below 1.2x your monthly expenses three times in 60 days, all non-essential automations pause.

Our recent analysis of savings automation adjustments found that people who build in circuit breakers like this are significantly less likely to slide into credit card debt during inflation spikes. The automation should protect you, not work against you.

A simple audit workflow helps keep this actionable:

Use this workflow as a checklist each month while inflation is volatile.

Expense elasticity scoring—know what can actually flex

Not all expenses behave the same way during inflation. Some are locked, some are sticky, and some are genuinely flexible. But there's a fourth category that trips people up: expenses that look elastic but aren't.

Score every expense line on true elasticity:

| Category | Flex |

|---|---|

| Locked (0% flex) | Rent, mortgage, insurance, loan minimums |

| Sticky (10% flex) | Utilities, phone, internet, necessary subscriptions |

| Semi-elastic (30% flex) | Groceries, gas, clothing, personal care |

| Fully elastic (90% flex) | Entertainment, dining out, hobbies, optional subscriptions |

The semi-elastic category is where inflation hits hardest. These are necessary enough that you can't eliminate them, but flexible enough that prices can spike without any protection. This is exactly where your tactical reserve does its work.

The short-term goal triage nobody wants to do

You had a plan. Down payment saved by 2027. European trip in September. New car when the lease ends. Those goals made sense in January.

Run this calculation for every short-term goal:

Current progress ÷ (Monthly contribution × Remaining months) = Completion probability

Adjust the monthly contribution for your new reality, then add 8% to the goal amount for inflation. That $40,000 house down payment? Probably $43,000 now. That $500 monthly contribution? After your June 2026 budget adjustments, maybe it's $300.

Most goals will fall into three buckets:

Green light goals: On track even with adjusted contributions. Keep these running, monitor monthly.

Yellow light goals: Possible but tight. Need active management and probably some hard trade-offs.

Red light goals: Mathematically impossible without major sacrifice. Pause, postpone, or reimagine these.

The psychological hit of pushing a goal from 2027 to 2028 is real. The financial hit of forcing an impossible goal is worse.

Building your inflation dashboard

Four numbers, visible every week:

-

Burn rate reality Actual last-30-days spending divided by 30

-

Automation burden Total monthly automated transfers as a percentage of net income

-

Tactical reserve days Reserve balance divided by daily burn rate

-

Inflation gap Current month spending minus same month last year

Track these in whatever system you're already using—spreadsheet, app, notebook. Doesn't matter. What matters is weekly visibility. Monthly is too slow when inflation is this volatile.

When burn rate reality exceeds 95% of net income for two consecutive weeks, hit the emergency brake on all non-essential automations. When automation burden exceeds 35% during inflation, you're probably overcommitted. When tactical reserve drops below 30 days, rebuild it before anything else.

The reconciliation ritual that prevents drift

Every Sunday night, 12 minutes:

-

Check actual spending versus last week's plan (3 minutes)

-

Flag any category that's 15% over budget (2 minutes)

-

Adjust next week's discretionary spending by the overage (3 minutes)

-

Move money between accounts to reset tactical reserve if needed (2 minutes)

-

Make one automation adjustment if triggered (2 minutes)

This isn't budgeting. You already have a budget. This is making sure reality and plan stay connected when inflation's pushing them apart.

There's a real opportunity here for operational software to do a lot of this monitoring automatically—flagging divergence before it becomes a crisis, suggesting specific automation tweaks based on actual spending patterns versus inflation trends. Until that's widely accessible, the Sunday night ritual is the next best thing.

When to reverse course

This entire framework is temporary. You're not permanently cutting retirement contributions or carrying inflated emergency fund targets forever.

Set clear restoration triggers:

-

Inflation drops below 3% for two consecutive quarters

-

Income adjusts upward to match or exceed cumulative inflation

-

Tactical reserve goes untouched for 90 days

-

Core expenses stabilize for three consecutive months

When you hit two of these four, start unwinding. Restore retirement contributions first—compound interest doesn't wait. Then rebuild depleted goal funds. Then reduce the emergency fund back to normal levels once stability looks confirmed.

The mistake people make is either overreacting (canceling everything) or underreacting (changing nothing). The goal is calibrating your response to the actual severity of your situation, not the headlines.

June's CPI numbers aren't the end of the world, but they're not nothing either. Your money management system needs to acknowledge that and adjust. The automation you built six months ago needs some manual attention right now. That's not failure—it's just staying honest with your finances.

Start with the automation audit today. Those transfers are hitting your account whether you're ready or not.

Ready to master your money?

Join thousands of users leveraging Savioly to build smarter budgets, save more efficiently, and plan for a secure financial future.