The freelance designer who runs their business out of a single checking account usually discovers the problem in March. Tax season hits and suddenly they're surrounded by receipts, printed bank statements, trying to figure out which Venmo payments were client income and which coffee stops were actually business-related versus just... coffee. Micro entrepreneur cash separation doesn't require accounting software or business entities. What most sole proprietors actually need is a dead-simple system that takes maybe 20 minutes a month to maintain and completely prevents that March disaster.

Why traditional separation advice fails for micro-businesses

Standard advice says open a business checking account, get a business credit card, track everything in QuickBooks. Solid advice if you're pulling $10k+ monthly. For someone doing $2-4k in side income? The $30 monthly fees and hours of bookkeeping feel completely out of proportion.

The real challenge isn't separation itself — it's finding something light enough that you'll actually stick with it. Most micro-entrepreneurs abandon their "proper" bookkeeping setup after two or three months because the overhead doesn't match their scale. What works better is a percentage-based model that scales with income. No fixed fees eating into slow months. No complex categorization. Just simple splits that happen automatically.

The percent-split framework that actually works

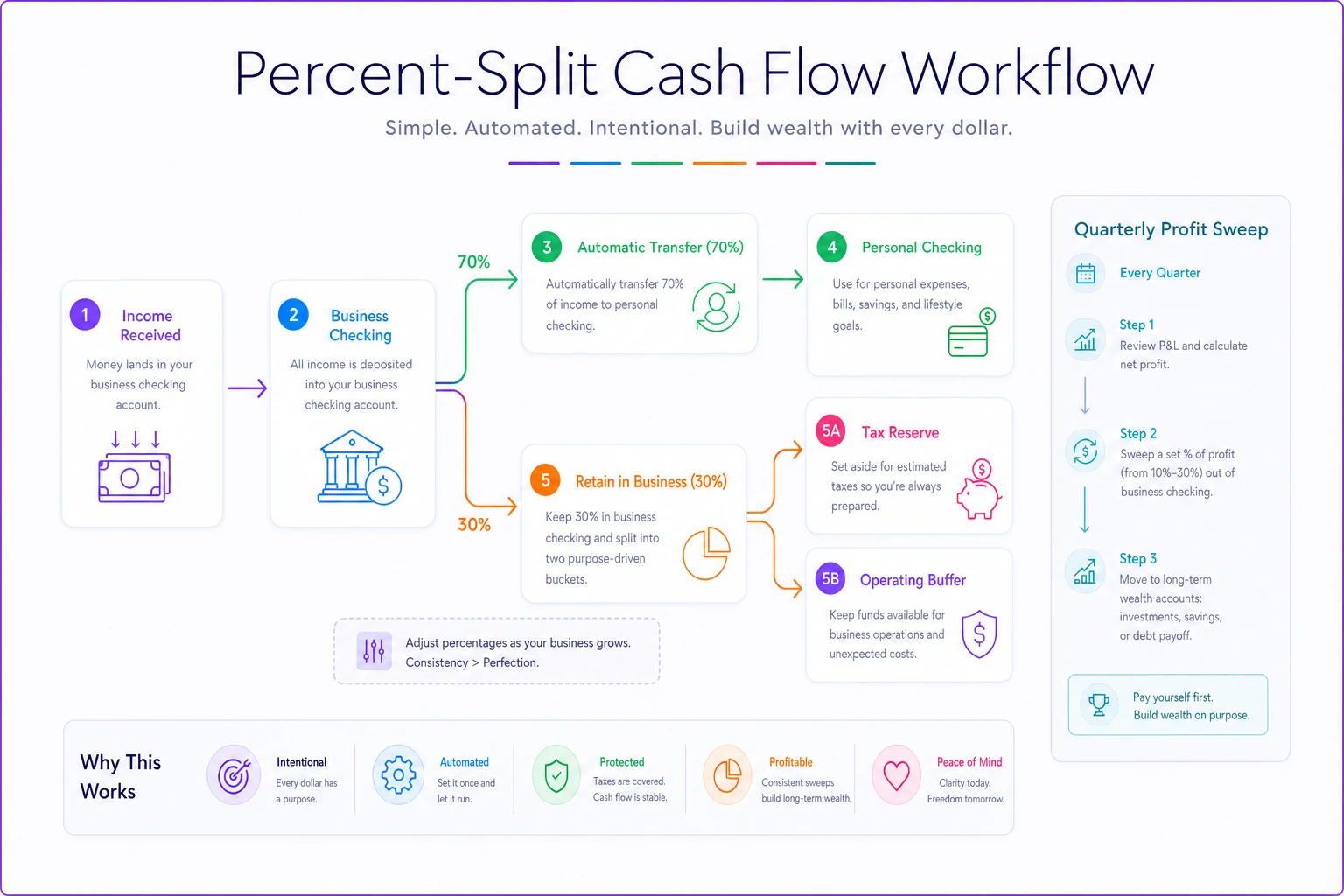

Basic account structure:

Take charge of your finances with clarity and confidence.

Savioly gives you real-time visibility and actionable steps to improve your money management.

- Automated expense tracking

- Goal-based saving plans

- Personalized financial insights

No credit card required

-

Personal checking (existing)

-

Business checking (free online option)

-

Single "float" savings account

The split formula:

-

Everything lands in business checking first

-

Calculate owner draw

(Total income × 70%)

-

Transfer that 70% to personal immediately

-

Leave 30% in business for taxes and expenses

The 70/30 split handles most micro-business realities — you're taking home enough to live on while keeping enough buffer for quarterly taxes (usually 15-25% for self-employment) plus some operating cushion.

For different income levels or expense profiles, adjust accordingly:

| Monthly Income | Suggested Split | Tax Reserve | Operating Buffer |

|---|---|---|---|

| Under $3k | 75/25 | 20% | 5% |

| $3k-$6k | 70/30 | 25% | 5% |

| $6k-$10k | 65/35 | 28% | 7% |

| Over $10k | 60/40 | 30% | 10% |

Don't overthink the percentages. Pick one, run it for three months, then adjust based on what actually happened.

A quick visual of the flow helps make the process feel actionable and easy to follow.

Owner pay rules that prevent cash crunches

The biggest mistake micro-entrepreneurs make with separation is taking money out randomly whenever they feel like it. This creates two problems: you lose track of profitability, and you eventually hit a tax bill you can't cover.

Fixed draw schedule: Pick two days per month for owner draws — first and fifteenth work well. On those days only, you transfer your accumulated 70% to personal. It creates natural spending discipline without feeling restrictive.

Emergency override rule: One condition where you can break the schedule: true emergencies over $500. Not concert tickets. Medical bills, car repairs that prevent you from working, actual crisis situations. Track every override in a note on your phone. If you're overriding more than once per quarter, your percentage split is probably off.

Profit sweep timing: Every quarter, after setting aside tax payments, sweep excess profit to personal. Only after taxes are covered. This becomes the reward for maintaining discipline — a quarterly bonus you've genuinely earned.

The monthly reconciliation that takes 20 minutes

Complex bookkeeping kills micro-business cash management. You need something you can knock out over coffee on a Sunday morning, not a weekend project.

Monthly checklist (set a recurring calendar reminder):

-

[ ] Download business checking statement

-

[ ] Highlight any personal expenses (usually 2-3 items)

-

[ ] Calculate total highlighted amount

-

[ ] Transfer that amount from personal to business

-

[ ] Check tax reserve balance (should be ~25% of total income)

-

[ ] Note current profit margin in phone

(Income - Expenses) ÷ Income

-

[ ] Done

No categorizing hundreds of transactions. No software. Just a quick scan for personal expenses that leaked into business, a transfer to fix it, and a sanity check on taxes.

The three numbers that matter:

-

Total income

-

Tax reserve balance

-

Profit margin

Everything else is noise at this scale. These three numbers tell you whether the business is working and whether you're prepared for tax season.

When to add complexity (and when not to)

Most micro-entrepreneurs add bookkeeping complexity too early. It creates overhead that kills momentum.

Add a business credit card when:

-

Monthly revenue consistently exceeds $5k

-

You have recurring business subscriptions

-

You're reimbursing expenses regularly

Until then, use your business debit card or pay directly from business checking. The rewards points aren't worth another account to reconcile.

Add bookkeeping software when:

-

You have multiple income streams

-

You're sending invoices regularly

-

You're approaching $50k annual revenue

Before that point, a basic spreadsheet works fine. Don't let perfect bookkeeping prevent good-enough separation.

Add an LLC when:

-

You have significant personal assets to protect

-

You're hiring contractors or employees

-

Your accountant specifically recommends it

Not because some blog post said you need one to be legitimate. The operational overhead isn't worth it under $30-40k annual revenue for most businesses.

Common separation mistakes that create tax disasters

The freelance writer who mixed personal and business money all year typically runs into three painful problems during tax prep: they can't prove deductions, they didn't save enough for taxes, and their profit looks worse than reality because personal expenses inflated their business spending.

The Amazon problem: Ordering business supplies through your personal Prime account seems fine until you're sorting through 200 orders to find the twelve that were actually business-related. Fix it the other way — use your business card for Amazon, then reimburse personal items monthly.

The Venmo/PayPal mess: Client pays through Venmo. You buy lunch through Venmo. Friend pays you back through Venmo. Now every transaction needs investigation. Business income should only go to business payment methods. Tell clients your Venmo is personal. Get a separate PayPal or use invoicing software that deposits directly to business checking.

The "I'll sort it out later" trap: Dumping everything into one account planning to separate it at year-end never actually works. By December you've forgotten what half the transactions were. Those client dinners look identical to date nights. That software subscription might have been business or personal streaming. The mental burden makes you give up and estimate, which costs you legitimate deductions.

Building habits that stick without constant willpower

The system only works if it becomes automatic. Relying on discipline for every single transaction is exhausting.

Transaction rules that eventually become muscle memory:

-

Client payments

Always to business checking, no exceptions

-

Business expenses

Always from business account or business debit

-

Personal purchases

Never from business accounts, even temporarily

The first month feels awkward. By month three, it's just how you operate.

The weekly five-minute scan: Every Friday, open your business banking app and scroll through transactions. Not to categorize or reconcile — just to notice what's there. This informal review catches personal expenses before they pile up and keeps your tax reserve visible without requiring any real effort.

It also makes the monthly reconciliation faster. You're already familiar with the transactions when you sit down to actually do the books.

Setting up guardrails: Link your business checking to Mint or your bank's own app, but only to flag obvious personal expenses. Restaurants, entertainment, shopping — set alerts for those categories. When they show up in business accounts, you know to look closer.

Some operational software can help by automating the separation of expenses into business and personal categories, but at micro-business scale, the manual scan takes so little time that automation sometimes adds more complexity than it removes.

Real numbers: what this looks like in practice

A virtual assistant doing $3,500 monthly with the 70/30 split:

Money in: $3,500 hits business checking

Immediate split:

-

$2,450 to personal (70% owner draw)

-

$1,050 stays in business (30% operations/tax)

Month-end breakdown:

-

Tax reserve

$875 (25% of gross)

-

Operating buffer

$175

-

Personal draw taken

$2,450

Quarterly tax payment: $2,625 Remaining profit to sweep: $525

Clean, simple, no surprises come April.

Compare that to the typical mixed-account situation where that same VA has $4,000 sitting in personal checking, no idea how much to save for taxes, and a March panic when the IRS wants $3,500 and there's only $800 saved.

The uncomfortable truth about micro-business money management

Most micro entrepreneur cash separation advice is written for a business that doesn't exist yet — some future version making $15k monthly with real operational complexity. That advice creates enough friction that a lot of people never get there.

The percent-split system isn't perfect. Professional bookkeepers would probably cringe at how simple it is. But it works because you'll actually do it. Imperfect separation beats perfect commingling every time.

Start with the basic three-account structure. Run percentage splits for one quarter. Do the monthly reconciliation even if it feels unnecessary at first. Build from that foundation as revenue grows.

The goal isn't pristine books that would impress an auditor. It's clean-enough separation so tax season doesn't ruin your spring, and so you actually know whether your business is profitable. Everything else is optional complexity you can add when the business genuinely needs it.

That freelance designer panicking in March? With this system, they'd spend 20 minutes pulling business statements, maybe another hour organizing receipts, and file with confidence. No archaeological expedition through mixed transactions. No guessing at deductions. No surprise bills. Just separation that scales with income and doesn't pretend a side hustle needs enterprise bookkeeping to function.

Ready to master your money?

Join thousands of users leveraging Savioly to build smarter budgets, save more efficiently, and plan for a secure financial future.