Most people fund their HSA, pay medical bills immediately, and move on. They're leaving thousands on the table—not because they don't understand the tax benefits, but because nobody's actually shown them how to run an HSA like an investment vehicle.

The real optimization playbook isn't about knowing that HSAs are tax-advantaged. Everyone knows that. It's about building decision rules for when to reimburse versus when to let money compound, creating a receipts system that still holds up five years from now, and knowing exactly when your balance tips from emergency fund to retirement accelerator.

People who build simple operational rules around their HSA consistently end up with more at retirement than those who just use it as a medical checking account. Not through complex strategies—through basic thresholds and timing rules anyone can follow.

The $3,000 Custody Threshold That Changes Everything

HSAs have this weird hybrid structure where part sits in cash and part can be invested. Most providers require you to keep somewhere between $1,000 and $2,000 in the cash portion before investing anything. But that's not really the number that matters.

The real shift happens at $3,000 total balance.

Below $3,000, your HSA should function as a pure medical emergency fund. Don't think about investments, don't hoard receipts for future reimbursement—just build a health expense buffer. Pay bills as they come, keep contributing, don't overthink it.

Between $3,000 and $7,500, you're in a transition zone. This is where selective reimbursement starts making sense—paying small stuff out of pocket (under $200 or so) while using HSA funds for anything bigger. You're also starting to invest whatever exceeds your cash threshold, even if it's just a few hundred dollars at first.

Above $7,500, the HSA becomes something different. Now you're paying everything out of pocket when possible, saving every receipt, and treating HSA disbursements as a last resort. The invested portion starts compounding meaningfully—returns you'll never pay taxes on.

One couple hit the $7,500 threshold after three years of maxing contributions. They shifted to paying all medical expenses out of pocket and investing everything above $2,000 in cash. Five years later, their HSA balance sat at $31,000 with $6,800 in saved receipts they could reimburse anytime. That's $6,800 of accessible tax-free money while the rest keeps compounding.

Reimbursement Timing Heuristics Without the Tax Complexity

The IRS lets you reimburse qualified medical expenses from your HSA anytime after you establish the account—even decades later. Most people completely ignore this.

Take charge of your finances with clarity and confidence.

Savioly gives you real-time visibility and actionable steps to improve your money management.

- Automated expense tracking

- Goal-based saving plans

- Personalized financial insights

No credit card required

Traditional advice says save all receipts and reimburse in retirement. That's not operationally realistic for most people. These timing rules hold up better in practice:

The Current Year Rule: For expenses under $200, reimburse within the same calendar year or just pay out of pocket. Tracking a $35 prescription for twenty years isn't worth it.

The Major Expense Float: For expenses over $1,000, save the receipt but don't reimburse for at least 18 months. This gives your invested HSA funds time to potentially grow past the expense amount. A $2,000 dental procedure becomes roughly $2,200 after eighteen months at 7% returns—that's $200 of tax-free gains you'd otherwise miss.

The Strategic Pull Trigger: Keep a running total of unreimbursed expenses. When that number hits around 20% of your total HSA balance, you've built a meaningful pool of tax-free money you can tap whenever you want. Below that threshold, let it ride.

Every unreimbursed medical expense essentially becomes a future tax-free withdrawal option. You're creating accessible tax-free liquidity while the actual HSA dollars keep growing.

A software developer accumulated $4,200 in unreimbursed expenses over four years while his HSA grew to $22,000. When he needed cash for a house down payment, he pulled that $4,200 tax-free instead of raiding his 401(k) or selling taxable investments. The remaining $17,800 kept compounding.

The Invest vs Pay Decision Template

Every medical expense triggers a decision: pay from HSA, pay out of pocket, or some mix. Without clear rules, you'll default to whatever feels easier in the moment—and that usually costs you over time.

| HSA Balance | Expense Amount | Your Decision | Why |

|---|---|---|---|

| Under $3,000 | Any amount | Use HSA | Building emergency buffer matters more than investing |

| $3,000–$7,500 | Under $200 | Pay out of pocket | Small expenses aren't worth tracking long-term |

| $3,000–$7,500 | Over $200 | Use HSA | Preserve cash flow while building HSA |

| Over $7,500 | Under $500 | Pay out of pocket | Let HSA compound, save receipt |

| Over $7,500 | $500–$2,000 | Check cash reserves first | If you have 3+ months expenses saved, pay out of pocket |

| Over $7,500 | Over $2,000 | Mixed approach | Pay what you can out of pocket, HSA for the rest |

The critical thing: your decision changes based on both your HSA balance and your overall financial situation. Someone with $50,000 in emergency savings should almost never touch their HSA for current expenses. Someone with $2,000 in savings needs that HSA as actual health insurance.

This template eliminates the paralysis. You know what to do when that $400 lab bill arrives or when you're staring at a $3,000 surgery estimate.

Simple Receipts-Tracking Cadence That Actually Survives Real Life

The biggest HSA optimization failure isn't bad investing decisions—it's receipt systems that fall apart after six months. You need something that works when you're busy, stressed, or just haven't thought about your HSA in three months.

Forget apps, forget complex spreadsheets, forget scanning every receipt.

-

The Folder System

Create one physical folder and one Google Drive folder labeled "HSA Receipts [Year]". Physical receipts go in the physical folder, email receipts get saved as PDFs in the digital folder. No categorization, no data entry, just dump and move on.

-

The Quarterly Sweep

Every expense category audit session, spend fifteen minutes updating a simple spreadsheet with four columns: Date, Provider, Amount, Running Total. Takes less time than brewing coffee and prevents the year-end scramble.

-

The Annual Snapshot

Each January, take a photo of your spreadsheet's running total and save it in your digital folder. Print the spreadsheet, staple it to that year's receipts, done.

Set a recurring calendar reminder tied to your Quarterly Sweep so it actually happens.

Even if you completely abandon this system for two years, you can reconstruct everything from your folders in an afternoon. No app subscriptions, no complex categorization, no passwords to forget.

A teacher using this approach accumulated seven years of receipts totaling $11,000 in unreimbursed expenses. When her car died unexpectedly, she pulled $5,000 tax-free using receipts from three years prior, leaving $6,000 in future reimbursement potential while her HSA balance kept growing.

The 65-Year-Old Transformation Nobody Mentions

At 65, your HSA undergoes a fundamental change that most optimization guides skip over entirely. You can withdraw money for any expense—not just medical—and only pay regular income tax, just like a traditional IRA.

Before 65, non-medical withdrawals trigger income tax plus a 20% penalty. After 65, that penalty disappears. Medical expenses still come out completely tax-free, but the overall flexibility increases significantly.

-

Stop saving receipts for expenses under $500 (not worth the hassle at that point)

-

Start using HSA funds for Medicare premiums, which are a qualified expense

-

Consider HSA withdrawals before touching your Roth IRA to preserve tax-free growth

-

Keep enough receipts to cover roughly one year of expenses as a backup

This is where early optimization actually pays off. That software developer who built up $22,000 by being selective about reimbursements—if he holds that pattern until 65, he's looking at somewhere in the range of $90,000–$100,000 in his HSA. Even accounting for inflation and increased medical costs, that's years of tax-free medical expenses in retirement, or penalty-free regular income when needed.

Most people don't think about the 65 transition until they're close to it. The ones who understood it at 40 made different decisions along the way—and those decisions compounded into something meaningful.

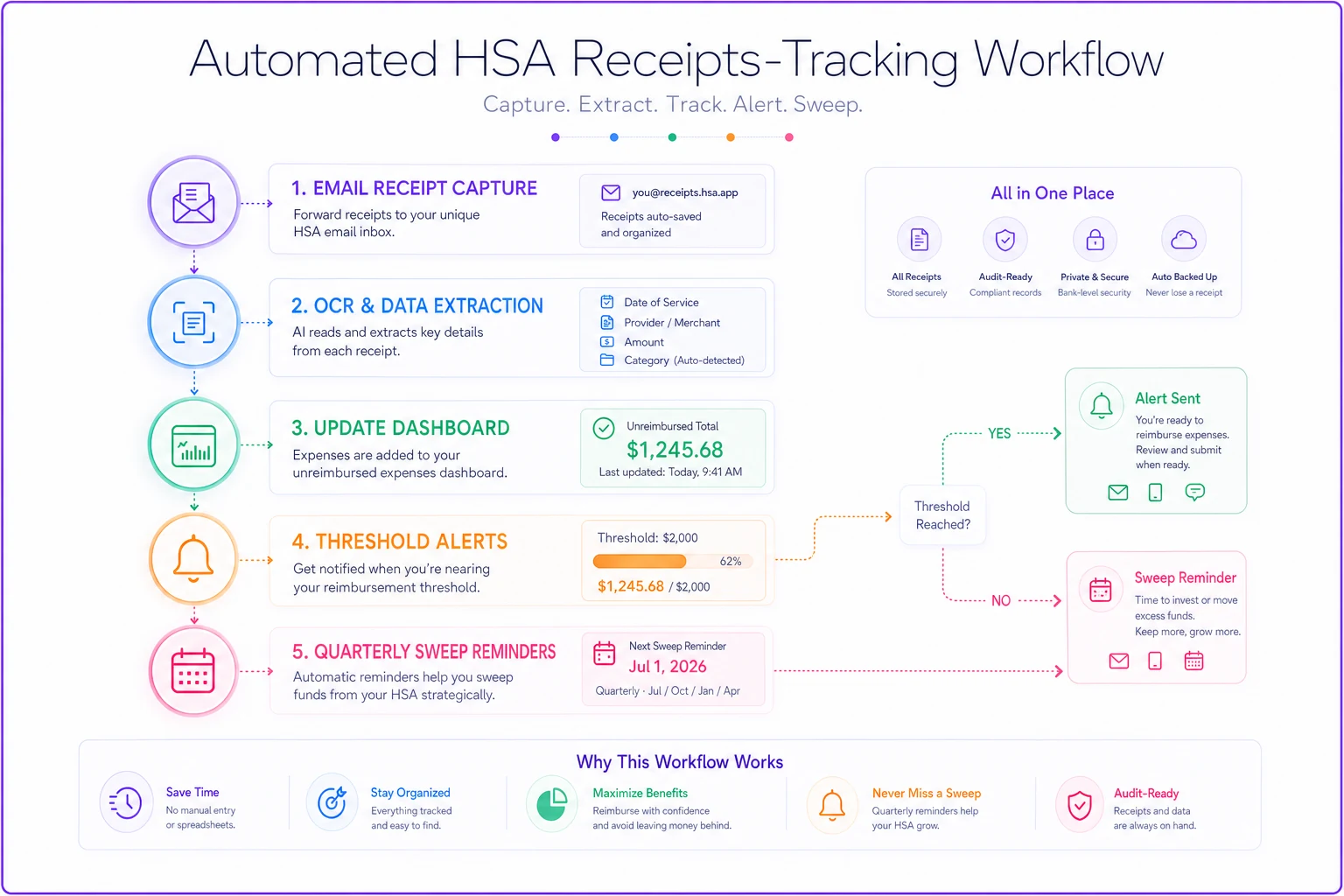

When Operational Software Makes HSA Tracking Effortless

The receipt tracking system above works, but it still requires manual quarterly sweeps and annual summaries. For people managing businesses or navigating multiple income scenarios, adding another financial tracking task can feel like a stretch.

This is where AI-powered operational software starts to make a real difference. Modern platforms can automatically capture email receipts, pull out amounts and providers, and maintain your running unreimbursed expense total without manual entry. More usefully, they can flag when you hit optimization thresholds—like when your unreimbursed expenses reach 20% of your HSA balance, or when your balance crosses into a new investment tier.

The goal isn't to replace your decision-making. It's to remove the administrative friction that causes most people to quietly abandon HSA optimization after a year or two. When receipt tracking runs in the background and you get a clean monthly summary, you're far more likely to stick with the strategy for the decade-plus it takes to actually pay off.

Common HSA Mistakes That Cost Thousands

The same patterns keep showing up:

The Immediate Reimbursement Reflex: Someone gets a $300 medical bill and immediately submits for HSA reimbursement, even with $15,000 invested. That $300 could have grown to $600+ over ten years. Multiply this across dozens of small expenses and you're leaving serious money behind.

The Investment Paralysis: People wait until they have $10,000+ to start investing their HSA, thinking they need a large balance to make it worthwhile. But investing just $1,000 at age 30 becomes around $7,600 by age 65 at 6% returns. Starting early matters more than starting big.

The Receipt Amnesia: After diligently saving receipts for two years, people get busy and stop tracking. Then they assume those old receipts are worthless. They're not—those receipts remain valid indefinitely. That $2,000 in receipts from 2019 is still $2,000 you can withdraw tax-free today.

The Spouse Confusion: Married couples often don't realize they can use one spouse's HSA to pay the other spouse's medical expenses, even if only one has HSA coverage. This flexibility opens up options a lot of couples miss entirely.

These mistakes aren't about ignorance—they're about not having a system. Most people understand the HSA rules in theory but make reactive decisions in practice, and reactive decisions tend to be expensive ones.

Building Your Personal HSA Optimization Triggers

The framework above works, but you need to adjust the thresholds to fit your situation.

Start with your current HSA balance and divide it into tiers:

-

Emergency tier

First $3,000

-

Growth tier

$3,000 to 3x your annual deductible

-

Investment tier

Everything above 3x your deductible

Next, set your reimbursement threshold based on cash reserves:

-

Less than 3 months expenses saved

Reimburse anything over $200

-

3–6 months saved

Reimburse only above $500

-

6+ months saved

Pay everything out of pocket, save all receipts

Finally, set calendar reminders for:

-

Quarterly receipt sweeps (15 minutes)

-

Annual reimbursement review (30 minutes)

-

Investment rebalancing check whenever you max contributions

These triggers remove daily decision fatigue while keeping you on track for long-term growth.

The Bottom Line on HSA Optimization

Your HSA optimization approach doesn't need to be complicated. It needs to be operational—clear thresholds, simple tracking, and triggers that work with your actual life.

Treating your HSA like a medical checking account versus an investment vehicle is a difference that compounds hard over time. We're talking tens of thousands of dollars in additional retirement funds for someone who starts optimizing at 35. Not through fancy investing or tax strategies—through basic custody thresholds and reimbursement discipline.

Start with the $3,000 threshold. Build the folder system. Set your quarterly sweep reminder. Those three things alone put you ahead of most HSA holders.

Every dollar you don't reimburse today becomes several dollars in retirement. Every receipt you save creates future tax-free withdrawal optionality. Every investment threshold you hit accelerates the growth.

And this system survives real life. It works when you're busy, when you forget about it for a few months, when things get messy. The best optimization strategy is the one you actually stick with for decades—not the perfect one you abandon after six months.

Your HSA isn't just a medical savings account. With the right operational approach, it becomes one of the most powerful retirement vehicles available—triple tax-advantaged, completely flexible, and accessible when you actually need it.

Ready to master your money?

Join thousands of users leveraging Savioly to build smarter budgets, save more efficiently, and plan for a secure financial future.