The refinance calculators you find online lie by omission. They'll show you monthly payment differences and lifetime interest savings, but skip the part that actually creates the most damage: liquidity traps that force bad decisions later.

The pattern is pretty consistent. People who refinance at the wrong threshold end up cash-strapped within 18 months. Those who prepay without proper guardrails sacrifice investment returns that would've meaningfully moved their net worth. And almost everyone skips the sensitivity scenarios that actually determine which path makes sense.

The break-even formula that accounts for opportunity cost

Standard break-even math divides closing costs by monthly savings. If refinancing costs $4,800 and saves $200 monthly, you break even in 24 months. Simple, clean, and incomplete.

Real break-even analysis needs three additional elements:

Adjusted Break-Even = (Closing Costs + Lost Investment Returns) / (Monthly Savings - Tax Adjustment)

Take someone refinancing from 5.75% to 4.25%. Closing costs run $4,800. Monthly payment drops $285. But that $4,800 could earn 7% invested. Over 24 months, that's roughly $340 in lost returns. Meanwhile, lower interest means $62 less in monthly tax deduction.

-

Numerator

$4,800 + $340 = $5,140

-

Denominator

$285 - $62 = $223

-

True break-even

what looked like 23 months is actually 28 months

Five months might not sound like much, but it changes things when rates shift or life gets complicated.

Liquidity guardrails that prevent operational collapse

Every mortgage decision needs three liquidity checkpoints. Skip these and you'll eventually find yourself selling investments at a loss or taking high-interest loans just to cover an emergency.

Take charge of your finances with clarity and confidence.

Savioly gives you real-time visibility and actionable steps to improve your money management.

- Automated expense tracking

- Goal-based saving plans

- Personalized financial insights

No credit card required

Guardrail 1: Post-closing emergency fund After refinancing costs, keep 4 months of expenses liquid. Not 3. Not "I'll rebuild it." Four months, untouched, accessible immediately.

Guardrail 2: The 18-month projection Map your cash position 18 months out. Include known expenses — insurance renewals, tax payments, anything already planned. If refinancing puts you below $8,000 liquid at any point in that window, wait.

Guardrail 3: Income volatility buffer Variable income requires stricter limits. Commission-based workers need 6 months of expenses post-closing. Seasonal businesses need coverage through their slow period. Contract workers should keep their full runway calculation intact before touching mortgage decisions.

Keep your post-closing emergency fund in an account separate from escrow refunds so it's immediately accessible and not accidentally spent.

A software consultant earning around $115k annually with quarterly client payments learned this the hard way. Refinanced in March, saving $310 monthly. By November, two delayed invoices combined with the liquidity hit from refinancing forced them to liquidate retirement funds — $3,400 in penalties and taxes. The $2,480 they'd saved through lower payments was already gone.

Sensitivity scenarios that reveal the real decision

Static calculations assume nothing changes. Run these three scenarios before committing:

Scenario A: Rates drop 0.75% within 18 months If you refinance now at 6.5% and rates hit 5.75% next year, you're stuck choosing between refinancing again (another $4,800) or accepting you moved too early. Calculate the crossover point where waiting would've beaten acting.

Scenario B: Income drops 30% for 6 months Model this explicitly. Can you cover the new payment plus expenses on reduced income? Prepaying keeps flexibility — you can stop anytime. Refinancing locks you into the same payment regardless.

Scenario C: Investment returns exceed mortgage rate by 3% When your mortgage costs 5% but investments return 8%, every prepayment dollar costs you that spread. On a $300,000 mortgage, prepaying $500 monthly sacrifices roughly $180 monthly in investment returns — around $2,160 a year.

The prepayment sweet spot most people miss

Prepayment works best in specific windows. Outside them, you're not being disciplined — you're just burning money.

Zone 1: Years 5-12 of a 30-year mortgage Early enough that principal reduction still matters, late enough that you're actually hitting principal meaningfully. Before year 5, most of your payment is interest anyway. After year 12, the acceleration benefit drops off.

Zone 2: When mortgage rate exceeds safe investment returns by 1.5% If your mortgage costs 7% and bonds pay 5%, that spread justifies prepayment. When mortgages cost 4% and index funds average 7%, prepayment becomes expensive virtue signaling.

Zone 3: Within 7 years of retirement Eliminating mortgage payments before fixed income starts changes retirement math dramatically. A couple planning to retire in 2031 should probably start aggressive prepayment by 2024, even if returns take a slight hit.

Decision matrix with numeric triggers

Stop guessing. Use these thresholds:

| Current Rate | Market Rate | Liquid Assets | Action |

|---|---|---|---|

| Above 7% | Below 5.5% | >$25k after costs | Refinance |

| 6-7% | Below 5% | >$30k after costs | Refinance |

| 5-6% | Below 4% | >$35k after costs | Consider refinance |

| Below 5% | Any | <$20k | Prepay nothing |

| Below 5% | Any | >$50k | Prepay if rate exceeds investments |

| Any | Rising | >$40k | Lock prepayment schedule |

These aren't suggestions. They're thresholds based on what consistently goes wrong when people guess instead of calculate.

The investment alternative everyone miscalculates

Comparing prepayment to investment returns seems simple. It's not. Tax treatment, risk adjustment, and accessibility all change the math.

Prepaying a 5% mortgage creates a guaranteed 5% after-tax return. To match that with taxable investments, you need roughly 6.5% returns (assuming a 25% tax rate). But that ignores risk. Mortgage prepayment carries zero volatility. Stock investments might return 10% or lose 15% — sometimes in the same year.

The real formula:

Required Investment Return = Mortgage Rate / (1 - Tax Rate) + Risk Premium

For most situations:

-

5% mortgage

-

25% tax bracket

-

2% risk premium

-

Required return

5% / 0.75 + 2% = 8.67%

Only invest instead of prepaying when you're confident of consistently clearing that threshold.

Refinancing's hidden operational costs

Beyond closing costs, refinancing creates friction people forget to price in.

Payment timing shifts Your payment date changes, sometimes significantly. Auto-payments break. Budget cycles need adjustment. This creates 1-2 months of cash flow disruption that occasionally triggers overdrafts or missed payments elsewhere.

Escrow account gaps Old escrow refunds arrive 30-45 days after closing. New escrow needs funding immediately. That temporary $3,000-5,000 gap catches people who didn't keep adequate reserves.

Documentation overhead Paperwork, appraisals, underwriter requests — figure 15-20 hours total. A consultant billing $125 an hour loses over $2,000 in opportunity cost just managing the process.

When prepayment beats both refinancing and investing

Three situations make prepayment the right move regardless of rates:

Situation 1: Approaching debt ratio limits When you need to qualify for other financing soon — a business loan, investment property — reducing mortgage balance improves debt-to-income ratios more directly than refinancing.

Situation 2: Variable income with a high mortgage Commission-based sales, seasonal businesses, contract work — when income swings 40% or more monthly, the security of lower principal beats any return calculation.

Situation 3: Within 24 months of selling Refinancing won't hit break-even. Investment returns won't compound enough to matter. Prepayment directly increases sale proceedings dollar-for-dollar.

The coordination problem that breaks most plans

People treat these decisions in isolation. They refinance, then realize they can't fund quarterly tax obligations. Or they prepay aggressively, then need cash for an opportunity that comes up. These decisions connect to everything else in your financial picture.

Worth maintaining a simple decision log with:

-

Current mortgage

rate, balance, payment

-

Liquidity position

emergency fund, accessible investments

-

Income stability

variation percentage, contract timeline

-

Upcoming needs

major purchases, tax obligations, tuition

Review it quarterly. When any metric crosses a threshold, reassess all three options — refinance, prepay, invest. It sounds like more work than it is, and it prevents emotional decisions when rates move or a balance shifts unexpectedly.

Also worth reading: don't choose the wrong payoff — a hybrid avalanche/snowball debt roadmap if you're managing multiple obligations alongside your mortgage.

Practical implementation without constant recalculation

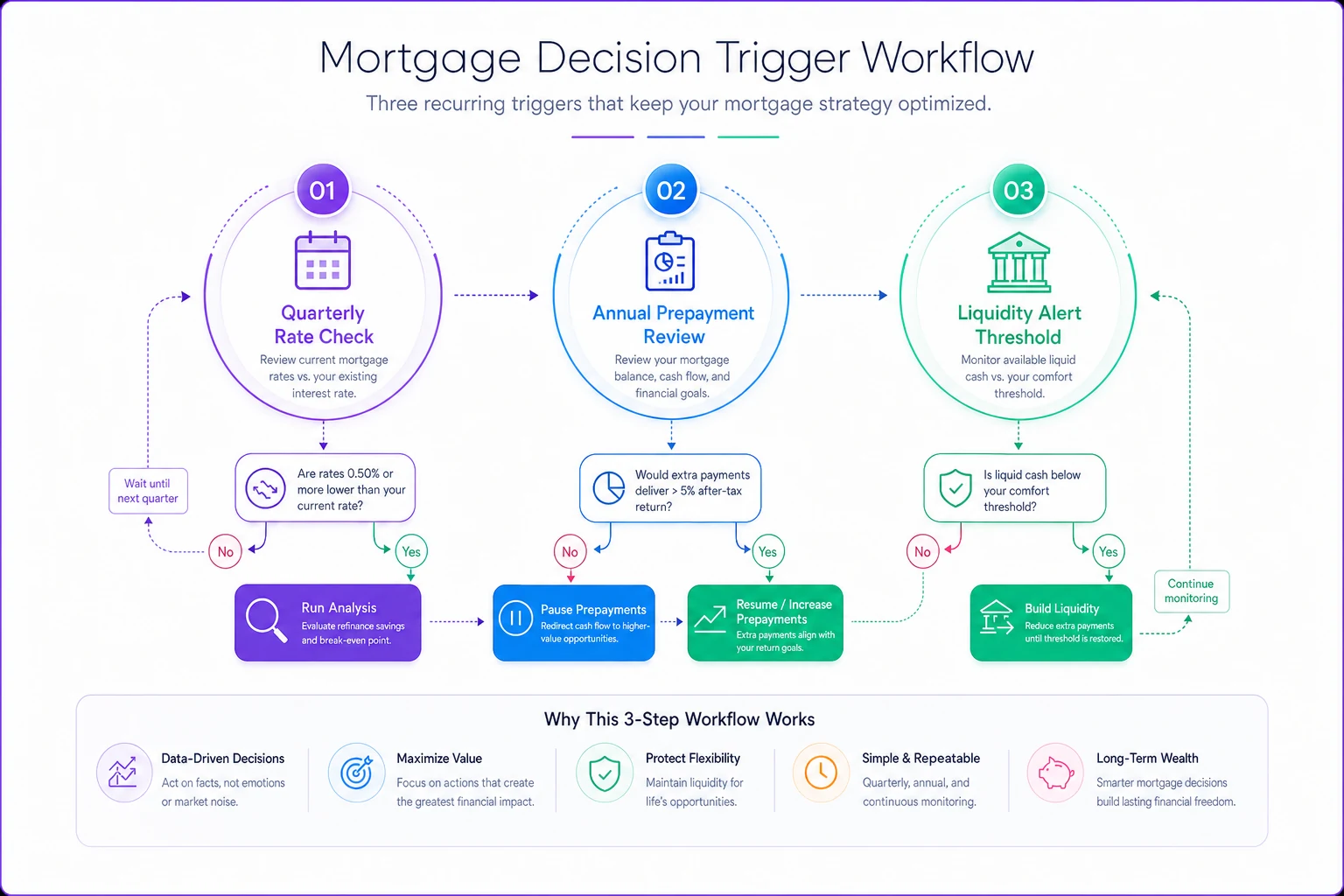

Set three triggers and ignore everything else:

Quarterly rate check When 30-year rates drop 1.25% below your current rate, run the full analysis. Otherwise, ignore rate headlines entirely.

Annual prepayment review Every January, calculate whether last year's prepayments would've earned more invested. Adjust accordingly.

Liquidity alert threshold When liquid assets drop below 5 months of expenses, stop all prepayments. When they exceed 8 months, resume or increase.

Here's a quick visual of the trigger workflow to keep the process clear.

These triggers remove daily decision fatigue while making sure you don't miss real opportunities. The system only works if you actually commit to it — checking rates every week because you saw a headline defeats the purpose entirely.

What this actually means for your mortgage strategy

The refinance-or-prepay question isn't binary. Most households do best with a dynamic approach: refinance when thresholds clearly favor it, prepay moderately during stable periods, invest when markets offer a clear premium over your mortgage rate.

The math matters, but the guardrails matter more. The households that avoided financial stress were almost always the ones who respected liquidity thresholds — not the ones who chased the last quarter-point of optimization. The ones who ignored those guardrails for marginally better returns usually regretted it within two years.

A 0.5% optimization on a $300,000 mortgage saves around $35,000 over the loan term. But losing liquidity at the wrong moment can cost more than that in penalties, forced sales, and missed opportunities — sometimes in a single year.

The households that win this game aren't the ones who perfectly time every refinance or max every prepayment. They're the ones who maintain flexibility, respect liquidity requirements, and make adjustments based on numeric triggers rather than market noise or what their neighbor just did. Run your numbers through these frameworks, set your thresholds, and execute consistently — the mortgage game rewards discipline over cleverness, every time.

The refinance-or-prepay question isn't binary. Most households do best with a dynamic approach: refinance when thresholds clearly favor it, prepay moderately during stable periods, invest when markets offer a clear premium over your mortgage rate.

Ready to master your money?

Join thousands of users leveraging Savioly to build smarter budgets, save more efficiently, and plan for a secure financial future.