Most people handle taxes backwards. They muddle through the year, maybe adjust their W-4 once if they remember, then scramble in March to figure out what they owe. By then it's too late to do anything except write a check or celebrate an unexpected refund that should've been in their pocket all year.

The mixed-income problem nobody talks about

Traditional tax advice assumes you're either a W-2 employee or self-employed. But that's not how real households work anymore. You've got a salary job, your spouse does consulting, you rent out the basement on Airbnb, maybe sell stuff on eBay when you declutter. Each income stream has different tax treatment, different timing, different withholding rules.

What happens in practice? People either massively overwithhold from their W-2 (giving the government an interest-free loan all year) or they ignore the problem entirely and hope their salary withholding covers everything else. Neither works.

One household I analyzed had a marketing manager making $78k salary, her husband doing contract UX work bringing in roughly $35k–45k depending on the year, plus around $800 monthly from a rental unit. Their first year doing taxes together, they owed $11,000. Not because they were irresponsible—they just had no system connecting these income streams to a unified tax provision.

The complexity isn't the math. Tax calculations are straightforward once you know the inputs. The complexity is operational: tracking multiple income sources, adjusting for irregular payments, and maintaining reserves without over-allocating cash you actually need for living expenses.

Why quarterly estimates fail for mixed households

The IRS wants self-employed income paid quarterly through estimated taxes. Makes sense for pure freelancers. For mixed-income households, it creates more problems than it solves.

Take charge of your finances with clarity and confidence.

Savioly gives you real-time visibility and actionable steps to improve your money management.

- Automated expense tracking

- Goal-based saving plans

- Personalized financial insights

No credit card required

First, the timing never aligns with actual cash flow. Your rental income hits monthly, your spouse's consulting checks arrive randomly, your bonus lands in December. Trying to calculate precise quarterly payments from this chaos adds stress without improving accuracy.

Second, quarterly estimates assume stable income. But contract work fluctuates. Side businesses have seasonal patterns. That Airbnb income drops when tourists leave town. You end up either overpaying early in the year when you need the cash, or underpaying and owing penalties.

Third—and this is what really breaks the system—quarterly estimates don't talk to your W-2 withholding. You're running two separate tax systems that should be coordinated. Most people don't realize you can adjust W-2 withholding to cover self-employment tax on other income. The IRS doesn't care where the money comes from, just that it arrives.

The reserve formula that actually works

Monthly Tax Reserve = (Total Monthly Income × Effective Rate) - W-2 Withholding

The key is using your actual effective tax rate from last year, not marginal rates or online calculators. Pull your prior year 1040. Take line 24 (total tax) divided by line 11 (AGI). That's your real effective rate including all deductions, credits, and complexity. For most mixed-income households, this lands somewhere between 18% and 26%.

Run this for that marketing manager couple. Their combined monthly income averages around $10,400 ($6,500 salary, $3,100 consulting, $800 rental). Their effective rate from last year was 22%. Monthly tax need: $2,288. The W-2 already withholds $1,420. So they need to reserve $868 monthly for the other income.

| Description | Value |

|---|---|

| Combined monthly income averages around $10,400 | ($6,500 salary, $3,100 consulting, $800 rental) |

| Effective rate from last year | 22% |

| Monthly tax need | $2,288 |

| W-2 already withholds | $1,420 |

| Need to reserve monthly | $868 |

That's it. No quarterly calculations. No separate buckets for federal versus state. One number to move into a tax savings account each month.

But most people see that $868 and think it's too much. So they reserve $500 "for now" and promise to catch up later. This never works. The reserve formula only functions if you actually follow it. Every month. No exceptions.

Small withholding adjustments that compound

The beauty of mixed-income tax provisioning is that you have multiple levers. Most people never touch their W-4 after starting a job. But small withholding adjustments can eliminate the need for large cash reserves.

Start with the Additional Withholding line on your W-4 (line 4c). Instead of reserving $868 monthly from our example, you could add $400 to your W-2 withholding and only need to reserve $468. This seems minor, but it changes the operational burden. Moving $468 monthly feels manageable. $868 feels like a mortgage payment.

For couples, optimize across both W-4s. If one spouse has steadier income, load more withholding there.

The math is simple. Take your monthly reserve need, divide by number of paychecks per month. If you're paid biweekly, multiply by 12 then divide by 26. That's your per-paycheck additional withholding.

Some people resist this because they want to "see" their full paycheck. But you're paying the tax either way. Better to never see the money than watch it leave your account manually each month. Same psychology as 401k contributions—what you don't see, you don't miss.

For couples, optimize across both W-4s. If one spouse has steadier income, load more withholding there. If one has better cash flow timing, adjust accordingly. The IRS views married filing jointly as one tax unit. Use that flexibility.

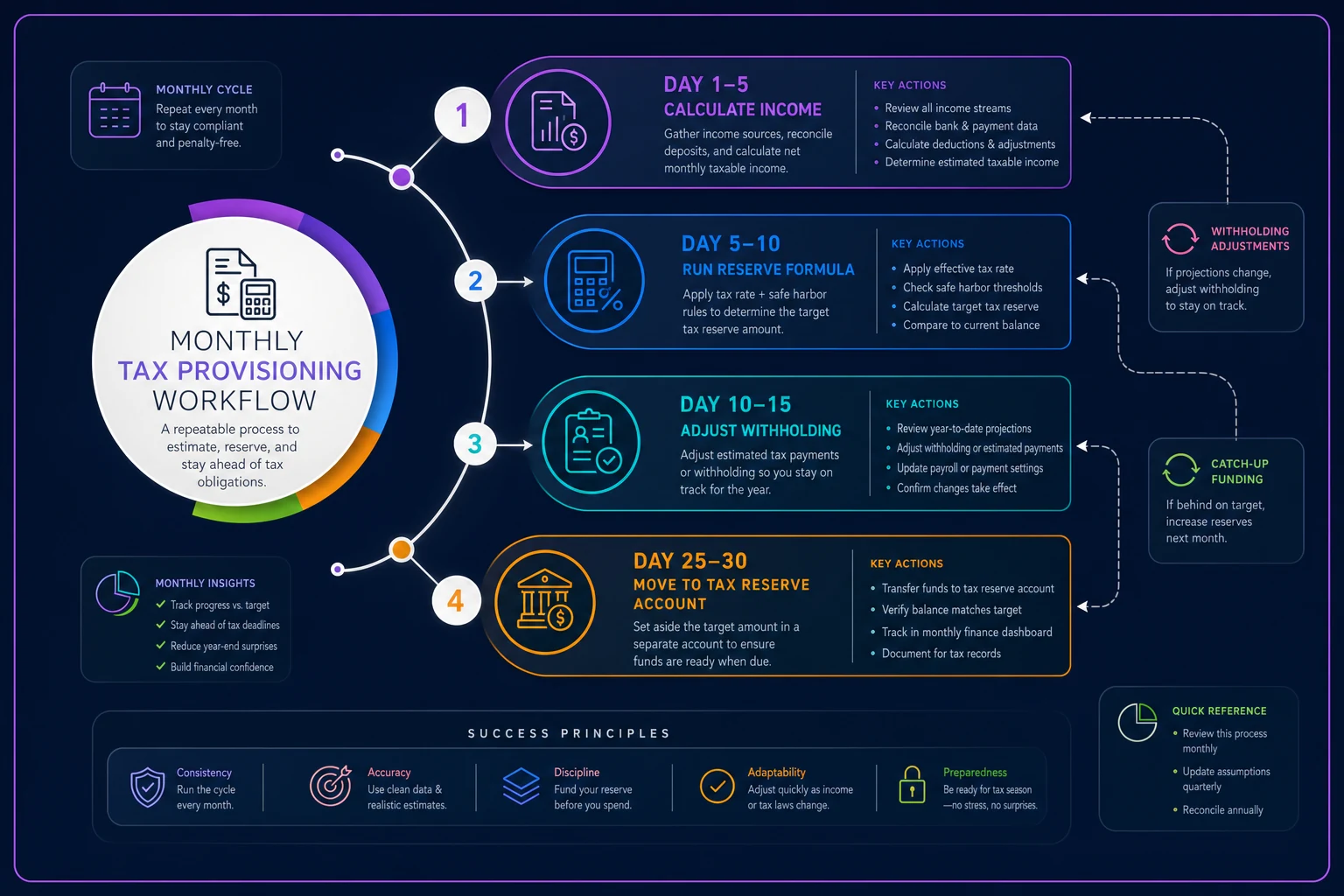

Monthly checkpoint cadence (not quarterly panic)

Running tax provisioning monthly changes the whole experience. You catch problems while they're small, adjust for income changes immediately, and never face a surprise bill in April.

Here's the monthly cadence that works:

Day 1–5: Calculate actual income from the previous month. Not estimates or averages—actual deposits that hit your accounts.

Day 5–10: Run the reserve formula. Compare required reserves to what you actually saved. If you're behind, you've got three weeks to catch up.

Day 10–15: Adjust next month's withholding if needed. Income trending higher? Add $50 to withholding. Big project cancelled? Reduce it.

Day 25–30: Move money to your tax reserve account. Physical separation matters—use a different bank if you have to.

This takes maybe 20 minutes monthly. Compare that to hours of stress in tax season, or the payment plan interest you'll pay if you can't cover your bill.

A simple visual can map this monthly workflow for quick review.

The checkpoint system also reveals patterns you'd miss otherwise. That side business might be more profitable in summer. Consulting work clusters around fiscal year-end. The rental needs major repairs every February. These patterns let you adjust provisioning ahead of time rather than reacting after the fact.

Automation templates for different household types

Most mixed-income households fall into one of a few patterns. Rather than building from scratch, start with a template that matches your situation:

The Side Hustler: W-2 job plus one irregular income source

-

Increase W-4 withholding by 30% of average monthly side income

-

No separate reserves needed if side income is under $1,000 monthly

-

Monthly checkpoint only when side income exceeds $1,500

The Power Couple: Two W-2s plus rental or investment income

-

Higher earner claims all dependents and deductions

-

Lower earner withholds at single rate with additional withholding

-

Reserve only for non-W-2 income

-

Quarterly checkpoint usually sufficient

The Transitioning Freelancer: Moving between W-2 and 1099 work

-

Maintain withholding at highest historical level

-

Reserve 25% of all 1099 income regardless of W-2 coverage

-

Weekly checkpoint during transition periods

-

Keep six months of tax reserves as runway

The Portfolio Builder: W-2 plus multiple investment or business streams

-

Baseline W-4 covers salary only

-

Separate reserve calculation for each income stream

-

Monthly aggregation and true-up

-

Consider quarterly estimates only if non-W-2 income exceeds $50k annually

These aren't rigid rules. They're starting points you adjust based on actual results. Pick one and run it for three months before tweaking anything. Most people constantly adjust their system without ever letting one approach prove itself.

When the formula breaks (and what to do)

No system handles every situation. The reserve formula breaks in predictable ways:

Massive income spike: You land a $30k project in November. The monthly formula says reserve 22%, but you know you're jumping tax brackets. Override it. Reserve 35% of windfalls over $10k.

First year of marriage: Your historical effective rate is useless when filing status changes. Use the IRS withholding calculator for year one, then switch to the formula once you have married filing jointly history.

Business losses: That rental property needs a new roof. Your side business bought equipment. Losses offset other income, but the reserve formula doesn't know this. Manually reduce reserves by 25% of deductible losses.

State tax complications: Moving states, working remotely, or earning income in multiple states breaks the single effective rate assumption. Run separate state calculations or add a 2–3% buffer to your formula.

The formula is a tool, not a religion. When circumstances change dramatically, adjust dramatically. Just document why you're overriding the system so you remember come April.

The AI-assisted tracking advantage

This is where modern tools make a real difference. Instead of manually calculating income, running formulas, and moving money around, AI-powered financial platforms can track your mixed income streams, calculate reserves in real-time, and initiate transfers automatically.

That marketing manager couple spending 20 minutes monthly on tax provisioning? With proper automation, they're checking a dashboard for 30 seconds to confirm everything's on track. The platform tracks all three income sources, adjusts reserves when consulting income spikes, and flags if they're falling behind.

AI automation also catches patterns that are easy to miss manually. Like how rental income drops every November when students leave for Thanksgiving, so reserves can be lower that month. Or how consulting work clusters in Q1, meaning January needs higher provisioning even when December was quiet. These small adjustments keep more cash available during lean months while making sure you're never caught short.

The better platforms connect directly to business and personal bank accounts, categorize income automatically, and maintain a running calculation of your effective tax rate. Tax provisioning stops being a monthly task and becomes a background operation that mostly runs itself.

Making it stick when life gets chaotic

Setting up tax provisioning is the easy part. Maintaining it when life gets messy is harder. Your kid gets sick, work explodes, the rental needs emergency repairs. Suddenly that monthly checkpoint feels impossible.

Build forgiveness into the system. If you miss a month, the next checkpoint runs a two-month calculation. Miss a quarter? The formula still works, just with a bigger catch-up number. The point isn't perfection—it's avoiding the April surprise.

A few things that actually help:

-

Set reserve transfers for the day after your largest regular deposit. It's easier to save when your account balance is high. For W-2 earners, that's usually payday. For freelancers, whenever your biggest client pays.

-

Start conservative and adjust down, not up. Better to over-reserve early and reduce later than scramble to catch up. If you're tracking toward a refund in October, reduce November and December reserves or leave them as a buffer for next year.

-

Connect provisioning to something you already do monthly. Pay rent on the first? Add tax checkpoint to that routine. Review credit cards monthly? Bundle it in. The best habits piggyback on existing ones.

And this matters more than people think: when it works, notice it. That first April when you write your tax check without stress, without scrambling, without a payment plan—that's a real win. Most people never get there. You've built something that handles financial complexity in the background while you focus on everything else.

Beyond the basics: optimizing for life changes

Once your provisioning system runs smoothly, you can start optimizing for bigger changes. Having a kid? Your effective rate's about to drop with the child tax credit—adjust reserves down by $150–200 monthly. Buying a house? First-year mortgage interest will slash your effective rate. Plan for the refund rather than over-reserving.

Your multi-year living plan should account for these tax impacts. Major life changes don't just affect expenses—they fundamentally alter your tax situation. The households that plan for both sides maintain stability through transitions that derail others.

Same principle with income changes. Getting promoted? Your marginal rate might jump, but effective rate rises gradually. The formula handles this automatically as long as you're using actual historical rates, not theoretical ones. Starting a business? First-year losses offset W-2 income. Don't reserve for income that won't be taxable.

The real value of monthly tax provisioning isn't just avoiding surprises. It's the confidence to make bigger financial moves. When your tax situation is handled, you can take the contract job, start the side business, or buy the rental property without dreading the tax consequences. The system adapts automatically.

The bottom line on individual tax provisioning

Tax provisioning for individuals isn't about becoming a tax expert or running complicated calculations. It's about building a simple operational system that runs in the background of your financial life. The reserve formula, monthly checkpoints, and strategic withholding adjustments turn taxes from an annual crisis into a solved problem.

For mixed-income households especially, this approach beats traditional quarterly estimates every time. You maintain flexibility, optimize cash flow, and avoid the surprise bills that derail your runway-based budgeting.

Start with your actual effective rate from last year. Run the formula monthly. Adjust withholding to minimize cash reserves. Check progress monthly, not quarterly. Use the templates as starting points, but adjust based on your reality. And when life gets complicated, let the system bend without breaking.

Tax provisioning is just operations. It's not about perfect accuracy or complex strategies. It's about a repeatable process that handles complexity without creating stress. Get the operations right, and taxes become just another monthly task that takes care of itself.

The households that master this don't have special financial knowledge. They just run better systems. And in a world where income sources keep multiplying and tax rules keep changing, good systems beat perfect knowledge every single time.

Ready to master your money?

Join thousands of users leveraging Savioly to build smarter budgets, save more efficiently, and plan for a secure financial future.