Most retirees stumble through their first year of decumulation because financial planning stops at the accumulation phase. You spend decades building the nest egg, then suddenly need to reverse-engineer forty years of saving habits into a withdrawal machine that has to balance taxes, account types, market conditions, and actual spending needs all at once.

The gap between theory and execution kills retirement plans. You know the 4% rule exists. You understand RMDs kick in at 73. You grasp that Roth conversions might help. But when Monday arrives and you need cash for groceries, which account do you tap? What if the market dropped 8% last month? Should you still convert that traditional IRA chunk to Roth when your taxable account is underwater?

Retirees need executable playbooks, not more theory. The same way a restaurant needs specific workflows for inventory management, you need concrete retirement decumulation rules that turn abstract tax concepts into monthly actions.

Why withdrawal sequencing breaks without clear triggers

Traditional withdrawal advice suggests a basic hierarchy: taxable accounts first, then tax-deferred, finally Roth. This kindergarten-level sequencing ignores market realities, tax bracket management, and the psychological grind of watching balances drop.

The real problem shows up when multiple variables collide. Your taxable account holds appreciated stocks you don't want to sell. Social Security hasn't started yet. Healthcare costs spike unexpectedly. The market tanks right when you planned that Roth conversion. Without clear decision trees, retirees either freeze or make panicked moves that inflate tax bills for years.

Consider a typical scenario: Margaret retires at 62 with $400k in a traditional 401(k), $180k in taxable accounts, and $95k in a Roth IRA. Standard advice says drain the taxable account first. But her taxable holdings include Apple stock bought in 2008 with massive embedded gains. Selling triggers capital gains that push her into higher brackets, potentially affecting Medicare premiums two years out. Meanwhile, she has five years before Social Security starts—a perfect Roth conversion window that disappears if she waits.

Market-adjusted withdrawal triggers:

-

If taxable account balance > 18 months expenses AND market down >15% from peak: Pull from traditional IRA instead

-

If taxable account balance < 12 months expenses

Rebalance from tax-deferred regardless of market

-

If sitting in 12% bracket with headroom

Convert traditional to Roth up to bracket ceiling

These aren't suggestions—they're executable commands that remove decision fatigue during volatile periods.

Building your monthly withdrawal checklist

Operational discipline in retirement means creating repeatable processes that run regardless of market noise or emotional state. Businesses that survive decades don't wing it each month—they follow systematic procedures that account for variability.

Take charge of your finances with clarity and confidence.

Savioly gives you real-time visibility and actionable steps to improve your money management.

- Automated expense tracking

- Goal-based saving plans

- Personalized financial insights

No credit card required

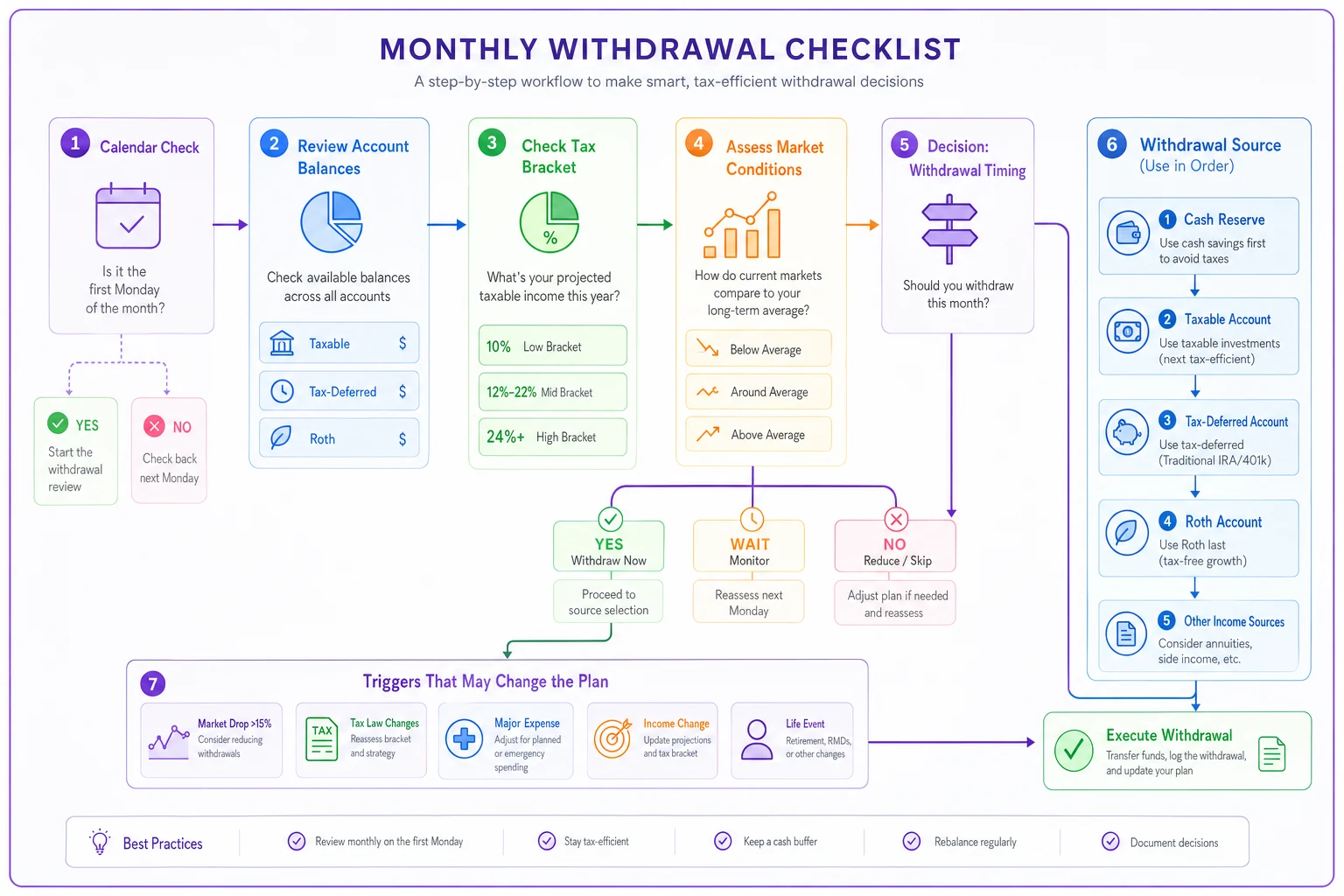

Your monthly withdrawal process should run like clockwork:

-

Calculate total cash needed for next 35 days (bills + discretionary + 10% buffer)

-

Check account balances across all three buckets

-

Review current tax bracket position year-to-date

-

Note market levels versus 12-month average

Withdrawal decision tree:

-

Cash reserves < 45 days? → Execute withdrawal immediately

-

Cash reserves 45-75 days? → Schedule withdrawal for mid-month

-

Cash reserves > 75 days? → Skip this month's withdrawal

Source selection (in order):

-

Dividends/interest sitting in cash (any account)

-

Maturing bonds or CDs

-

Taxable account positions with losses (harvest them)

-

Taxable account positions with <20% gains

-

Traditional IRA/401(k) if under RMD age

-

RMD amounts if applicable

-

Taxable account positions with >20% gains

-

Roth IRA (absolute last resort)

Use calendar reminders to run the checklist on the first Monday of each month.

Visual workflow of the monthly withdrawal checklist:

This checklist eliminates the "which account?" paralysis. You work down the list until you've sourced enough cash. No emotional decisions, no second-guessing.

Tax bracket management through deliberate fills

The biggest retirement tax mistake happens gradually—letting low-income years pass without doing anything strategic. Between retirement and RMDs lies a window where your tax bracket might be the lowest it'll ever be again.

Think of tax brackets like water glasses stacked at different heights. Your income fills the lowest glasses first. If you're only filling the 10% and 12% glasses during early retirement, you're wasting space that could be filled with Roth conversions or traditional IRA withdrawals.

Annual tax-fill strategy:

Every December, run this calculation:

-

Current taxable income for the year

$

-

Top of desired bracket (usually 12% or 22%)

$

-

Available "room" in bracket

$

-

Action

Convert or withdraw exactly that amount from traditional accounts

Example: Joe and Linda have $42,000 in taxable income for the year—pensions plus some dividends. The 12% bracket for married filing jointly tops out around $89,075. They have roughly $47,000 of room. They convert that amount from traditional to Roth in December, using up that low-tax space before it disappears.

Every December, you fill the bracket. The compound effect over 10-15 years of early retirement can save six figures in lifetime taxes. That's not optimization theater—it's basic operational discipline.

Real withdrawal scenarios for common account mixes

Theory crumbles when you're staring at actual account statements. Here's how retirement decumulation rules play out across typical portfolios:

| Scenario | Asset Mix | Monthly withdrawal guidance |

|---|---|---|

| Scenario 1: The Traditional-Heavy Retiree | 70% in traditional 401(k)/IRA; 20% in taxable accounts; 10% in Roth IRA | Pull primarily from traditional accounts while staying within your target tax bracket. Use taxable accounts only for large irregular expenses. Leave the Roth alone until RMDs push you into higher brackets—then use Roth withdrawals to avoid bracket creep. |

| Scenario 2: The Balanced Portfolio | 40% traditional; 35% taxable; 25% Roth | Alternate between taxable and traditional based on market conditions. Bull market—harvest taxable gains. Bear market—lean on traditional IRA. Use Roth strategically for years with unusual expenses (new roof, medical procedures) to avoid bracket jumps. |

| Scenario 3: The Roth-Converter | 20% traditional (rapidly shrinking); 30% taxable; 50% Roth | Live primarily on taxable account dividends and selective sales. Continue aggressive Roth conversions until the traditional balance reaches zero. After that, taxable for regular expenses, Roth for everything else. |

Scenario 1: The Traditional-Heavy Retiree

-

70% in traditional 401(k)/IRA

-

20% in taxable accounts

-

10% in Roth IRA

Monthly withdrawal: Pull primarily from traditional accounts while staying within your target tax bracket. Use taxable accounts only for large irregular expenses. Leave the Roth alone until RMDs push you into higher brackets—then use Roth withdrawals to avoid bracket creep.

Scenario 2: The Balanced Portfolio

-

40% traditional

-

35% taxable

-

25% Roth

Monthly withdrawal: Alternate between taxable and traditional based on market conditions. Bull market—harvest taxable gains. Bear market—lean on traditional IRA. Use Roth strategically for years with unusual expenses (new roof, medical procedures) to avoid bracket jumps.

Scenario 3: The Roth-Converter

-

20% traditional (rapidly shrinking)

-

30% taxable

-

50% Roth

Monthly withdrawal: Live primarily on taxable account dividends and selective sales. Continue aggressive Roth conversions until the traditional balance reaches zero. After that, taxable for regular expenses, Roth for everything else.

Each scenario demands a different operational rhythm. The traditional-heavy retiree needs careful bracket management. The balanced portfolio allows maximum flexibility. The Roth-converter accepts higher taxes now for simplicity later—and that tradeoff is intentional, not accidental.

Reforecast triggers that actually matter

Retirement plans die from rigidity. The 4% rule assumes you'll blindly withdraw the same inflation-adjusted amount regardless of crashes, health changes, or windfalls. Real systems include circuit breakers.

Mandatory reforecast triggers:

-

Portfolio down >20% from peak

- Reduce monthly withdrawal by 15% - Suspend all Roth conversions - Shift to bear market withdrawal sequence (traditional accounts first)

-

Portfolio up >30% from retirement date

- Recalculate safe withdrawal rate using current balance - Consider one-time lifestyle upgrade (capped at 10% increase) - Accelerate Roth conversions if under age 70

-

Major health diagnosis

- Project revised life expectancy - Front-load withdrawals if timeline is compressed - Maximize tax-advantaged medical payment strategies

-

Inheritance or windfall >$50k

- Pause all withdrawals for 3 months - Recalculate entire withdrawal strategy - Consider impact on tax brackets and Medicare premiums

These aren't annual review items—they're immediate action triggers. When conditions hit, you execute the prescribed response without debate. That removes emotional decision-making during precisely the moments when emotions run highest.

The spending smoothing system nobody explains

Retirees face a cruel paradox: expenses are lumpy but income needs to feel smooth. Property taxes hit twice yearly. Insurance premiums arrive annually. Cars need replacing. Yet most withdrawal strategies pretend every month looks identical.

The fix involves three spending buckets:

-

Monthly Fixed Rent/mortgage, utilities, groceries, regular medications

-

Quarterly Variable Property taxes, insurance premiums, estimated taxes

-

Strategic Reserve Car replacement, home repairs, medical procedures

Instead of scrambling when property taxes land, you pre-fund the Quarterly Variable bucket through slightly higher monthly withdrawals. If monthly expenses run $4,000 but quarterly obligations average $1,500, you withdraw $4,500 monthly and set aside that extra $500.

This smoothing system prevents the withdrawal panic that destroys tax efficiency. You never make rushed sales because a bill surprised you. Every expense becomes predictable at the operational level, even when the timing varies.

Common sequencing mistakes that compound

The worst retirement mistakes aren't dramatic—they're systematic errors that compound invisibly for years.

The RMD procrastination trap: Waiting until December to take RMDs forces year-end sales regardless of market conditions. Better approach: Take monthly RMD installments starting in January. This gives you flexibility if markets drop in Q4 and smooths out the tax hit across the year.

The Roth conversion cliff: Converting large chunks in single years spikes your tax bracket and Medicare premiums. Spreading conversions across 5-10 years keeps you in lower brackets throughout. Think marathon pacing, not sprinting.

The tax-loss harvesting abandonment: Many retirees stop harvesting losses because they're not working. But losses still offset gains and up to $3,000 of ordinary income annually. Systematic harvesting in taxable accounts creates tax assets you can deploy strategically.

The emergency fund oversight: Keeping twelve months of expenses in a checking account earning near nothing while simultaneously withdrawing from investment accounts makes zero operational sense. Your portfolio is your emergency fund in retirement. Keep 2-3 months in cash, invest the rest.

Creating your personal withdrawal command center

Build a simple spreadsheet with five tabs:

-

Tab 1

Account Balances - Update monthly - Track each account separately - Note cost basis for taxable positions

-

Tab 2

Withdrawal Log - Date, amount, source account - Running tax impact - Year-to-date totals by account type

-

Tab 3

Tax Bracket Tracker - Current year income by source - Distance to next bracket - Estimated taxes paid/owed

-

Tab 4

Trigger Dashboard - Market levels vs. triggers - Account balance ratios - Next required actions

-

Tab 5

Annual Strategy - This year's withdrawal plan - Roth conversion targets - Tax-loss harvesting opportunities

Update it monthly, review it before every withdrawal, adjust it when triggers hit. Modern financial planning software can automate much of this tracking—AI-powered platforms can monitor trigger conditions and flag optimal withdrawal sequences based on real-time tax situations. But whether you use sophisticated software or a basic spreadsheet, the point is having a system that removes guesswork from the monthly decision.

Your retirement shouldn't depend on remembering which account to tap or whether this month's market dip changes your strategy. Build the framework once, then execute it systematically. That's how you turn decumulation from a monthly anxiety into a boring, predictable routine.

For related reading on managing income uncertainty and debt strategy in the years leading up to or during retirement, see A Multi-Year Living Plan for Uncertain Incomes and A Hybrid Avalanche/Snowball Debt Roadmap.

The retirees who thrive don't always have better returns or bigger balances. They have better operations. They've turned the complex choreography of taxes, withdrawals, and market conditions into simple monthly procedures. Stop treating retirement withdrawals like one-off decisions. Start treating them like a system that needs proper infrastructure, clear triggers, and consistent execution.

That difference—between theory and operation—is the difference between retirement stress and retirement success.

Ready to master your money?

Join thousands of users leveraging Savioly to build smarter budgets, save more efficiently, and plan for a secure financial future.