Emergency funds sit in this weird psychological space where they're both essential and anxiety-inducing. Essential because unexpected expenses are basically guaranteed. Anxiety-inducing because every dollar sitting in that fund feels like it should be working harder — paying down debt, invested in the market, or funding that business idea you've been kicking around.

The real problem isn't whether you need an emergency fund. It's knowing exactly when to use it versus when to find alternative funding, and how to rebuild it without abandoning every other financial goal in the process.

The Decision Matrix Nobody Talks About

Most financial advice treats emergency fund usage like a binary decision — either it's an emergency or it isn't. But the actual decision process looks more like a multi-factor evaluation that happens in about thirty seconds of panic.

Your brain is simultaneously calculating: how urgent is this expense, can you float it on a credit card for 30 days, will depleting the fund trigger other problems, how long will rebuilding take, and what goals will have to pause. That mental math usually happens while you're staring at a repair estimate or a medical bill — which is exactly the wrong time to be making complex financial trade-offs.

Building Actual Trigger Rules

The solution is establishing clear drawdown triggers before you need them. Not vague guidelines about "true emergencies" — specific thresholds and conditions that remove decision fatigue when stress is high.

Take charge of your finances with clarity and confidence.

Savioly gives you real-time visibility and actionable steps to improve your money management.

- Automated expense tracking

- Goal-based saving plans

- Personalized financial insights

No credit card required

Immediate drawdown triggers (use emergency fund first):

-

Medical expenses exceeding $500 after insurance

-

Primary vehicle repairs required for work commute

-

Home repairs affecting habitability (not aesthetics)

-

Income loss exceeding 14 days

-

Legal obligations with deadlines

Alternative funding first (preserve emergency fund):

-

Predictable annual expenses you forgot to budget

-

Upgrades or improvements, even if they feel urgent

-

Travel for non-immediate family emergencies

-

Business investments or opportunities

-

Debt payoff acceleration

The key distinction: immediate drawdown triggers are situations where delay creates cascading problems. Alternative funding situations might feel urgent but won't compound if you take 48 hours to explore other options.

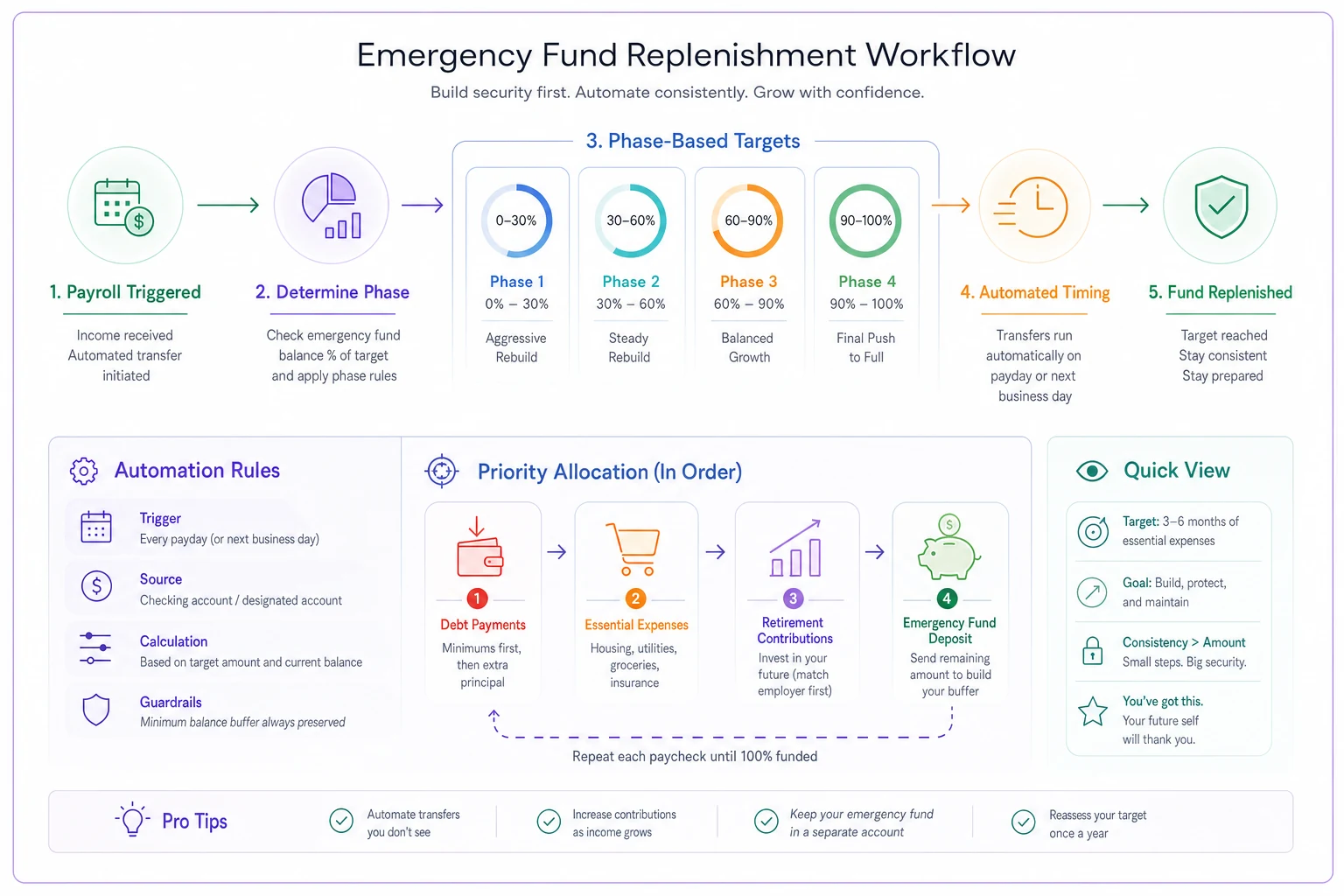

The Replenishment Sequence That Actually Works

This is where most emergency fund advice falls apart — the rebuild phase. Generic advice says "replenish as quickly as possible," which sounds responsible but ignores the reality that you probably had good reasons for your previous allocation strategy.

A prioritized replenishment sequence acknowledges that rebuilding happens alongside other financial obligations, not in isolation. The sequence adjusts based on your current stability level.

A quick visual of the phased rebuild workflow.

Phase 1: Crisis Prevention Mode (0–30% funded)

Allocation priority:

-

Minimum debt payments (maintain credit)

-

Essential living expenses

-

70% of discretionary income to emergency fund

-

30% to highest-interest debt

-

Pause all investment contributions except employer match

This feels extreme because it is. Below 30% funding, your next unexpected expense likely goes on a credit card at 24% APR — a mathematical emergency that supersedes optimization.

Phase 2: Stabilization Mode (30–60% funded)

Allocation priority:

-

Minimum debt payments

-

Essential expenses

-

50% of discretionary income to emergency fund

-

30% to debt above 7% interest

-

20% to retirement up to employer match

-

Pause additional investment contributions

The shift here: you're no longer in crisis mode, so some attention to high-interest debt and the employer match makes mathematical sense.

Phase 3: Balanced Rebuild (60–90% funded)

Allocation priority:

-

All minimum payments

-

Essential expenses

-

30% of discretionary income to emergency fund

-

30% to debt payments

-

30% to retirement/investments

-

10% to medium-term goals

This phase acknowledges that full emergency fund completion might take months, and completely pausing other goals creates its own risks.

Phase 4: Final Push (90–100% funded)

Allocation priority:

-

Standard expense coverage

-

40% of discretionary income to emergency fund

-

60% return to pre-drawdown allocation

The counterintuitive move here is temporarily increasing the emergency fund percentage. Dragging out the last 10% for months creates mental drag that bleeds into other decisions.

Payroll-Tied Automation Rules

Manual transfers to rebuild emergency funds fail for the same reason manual savings plans fail — decision fatigue and competing priorities. The fix is tying rebuilds directly to payroll cycles with rules that adjust based on fund levels.

Here's a functional automation structure:

| Fund Level | Transfer Timing | Notes |

|---|---|---|

| Under 30% | Immediately on payday | Prevents mental reallocation |

| 30–60% | Day 3 after payday | Allows minor cash flow flexibility |

| 60–90% | Day 7 after payday | Maintains momentum, less urgency |

| Over 90% | Resume normal allocations | Rebuild complete |

Set calendar reminders tied to payday to make manual transfers when your bank won't automate these rules.

The delays aren't random. Immediate transfers for crisis-level funding prevent the money from being mentally allocated elsewhere. Delayed transfers for higher funding levels allow cash flow flexibility while maintaining rebuild momentum.

Most banking apps can't handle this level of logic natively, but the manual version works: set calendar reminders tied to payroll dates with specific transfer amounts based on current fund percentage. Takes roughly 90 seconds every two weeks.

Goal Protection Mechanisms

The biggest psychological barrier to using emergency funds isn't the depletion itself — it's watching other financial goals stall. You finally had momentum on debt payoff, then suddenly you're back to minimums. Investment contributions that were becoming habitual are now paused indefinitely.

The 80% preservation rule: Never reduce goal contributions below 80% of target, even during rebuilds. If you were contributing $500 monthly to investments, maintain at least $100. If you were paying $300 extra on debt, keep at least $60 extra going. Complete cessation breaks psychological momentum and habit formation. Token contributions feel pointless, but the 80% threshold keeps goals mentally active while freeing up resources for rebuilding.

Time-boxed rebuild periods: Set a maximum rebuild timeframe regardless of fund level achieved — 3 months for drawdowns under $1,500, 6 months for drawdowns between $1,500 and $5,000, and 9 months for anything larger. After the time box expires, accept the achieved funding level and resume normal allocations. This prevents endless rebuild cycles that sacrifice long-term wealth building for theoretical security.

The compound protection calculation: Before any drawdown, calculate the true cost including rebuild opportunity cost. A $3,000 emergency fund drawdown doesn't cost $3,000 — it costs $3,000 plus several months of reduced investment contributions that could have compounded. Quick math: $3,000 drawdown plus 6 months reducing investments by $400/month equals roughly $5,400 of real cost before factoring in lost compound growth. Sometimes that calculation still favors using the emergency fund. Sometimes it reveals that a 0% promotional credit card or a personal loan actually costs less than the full rebuild cycle impact.

Rebuilding During Income Volatility

Standard rebuild rules assume stable income, but a meaningful chunk of workers deal with variable compensation — commissions, bonuses, seasonal work, self-employment. For variable income, the rebuild sequence needs buffer zones and percentage-based rules rather than fixed dollar amounts.

Below baseline month (under 80% of average): Pause emergency fund rebuilds entirely. Maintain minimum debt payments only and preserve cash flow flexibility.

Baseline month (80–120% of average): Standard rebuild percentage applies. Follow phase-based allocation priority as normal.

Above baseline month (over 120% of average): Accelerated rebuild — 50% of excess goes to emergency fund, remaining 50% follows normal allocation.

This creates automatic acceleration during good months without adding stress during lean ones. Percentages work better than fixed dollar amounts because they self-adjust to income reality.

For those with irregular income patterns, combining this approach with runway-based budgeting creates even more stability.

The Integration Problem

Where emergency fund rebuild rules typically break down is integration with existing financial systems. You've got automatic bill pay, investment transfers, debt payments, and savings allocations already running. Adding another layer of rules feels like juggling chainsaws.

The solution is treating rebuilds as temporary overrides, not permanent restructuring.

-

Keep existing automations running at reduced levels (the 80% rule)

-

Add temporary rebuild transfers as separate transactions

-

Set calendar reminders for phase transitions

-

Document the original allocation strategy before modifying anything

Once rebuilding completes, you're removing temporary transfers rather than trying to reconstruct an allocation strategy you half-remember from six months ago.

Software Solutions for Complex Rules

Managing multi-phase rebuild rules with various triggers and thresholds pushes spreadsheets past their practical limits pretty quickly. You need something that can evaluate conditions, trigger transfers, and adjust as fund levels change.

AI-powered financial management platforms handle this kind of operational complexity reasonably well. Instead of manually checking fund percentages and adjusting transfers every pay period, the platform handles evaluation and execution automatically — tracking phase transitions, time box expirations, and special condition triggers without requiring your constant attention.

More importantly, these platforms maintain visibility across all your financial goals simultaneously. While you're focused on rebuilding, the system tracks whether debt payoff is falling behind or if investment contributions need adjustment. That's the difference between juggling priorities in your head and having a dashboard that shows exactly where everything stands.

Common Rebuild Mistakes to Avoid

Rebuilding too aggressively: Throwing everything at emergency fund rebuilding often triggers burnout around month two. You end up either abandoning the rebuild or accumulating credit card debt for daily expenses, which defeats the purpose entirely.

Ignoring cash flow timing: Setting rebuild transfers for the day after payroll sounds logical but ignores that most bills cluster in the first week of the month. Transfer timing should account for your actual cash flow patterns.

Forgetting to restore original allocations: A surprising number of people who successfully rebuild their emergency funds forget to redirect those transfers back to their original goals. They end up with bloated emergency funds while wondering why debt payoff stalled.

Using windfalls incorrectly: Tax refunds and bonuses during rebuild periods need their own rules. The instinct is to dump 100% into the emergency fund, but maintaining some percentage for other goals prevents the psychological feeling of all sacrifice, no progress.

Special Circumstances Requiring Modified Rules

High-interest debt situations: If you're carrying credit card debt above 20% APR, standard rebuild rules don't apply. The math favors minimum emergency fund rebuilding — just enough to avoid additional debt — while aggressively paying down the high-interest balance. Once below 15% APR, standard rules resume.

Upcoming known expenses: If major expenses are approaching (annual insurance, tuition, planned medical procedures), the rebuild timeline needs adjustment. Either accelerate rebuilding before the expense or accept a longer timeline after.

Multi-income households: When partners have different income stability levels, rebuilds should prioritize stable income for emergency funding while variable income handles other goals. This reduces stress and maintains predictability during the rebuild phase.

Self-employment tax obligations: Emergency fund rebuilds compete directly with quarterly tax savings for self-employed people. The fix is straightforward — treat tax obligations as non-negotiable and rebuild with whatever remains. The IRS doesn't care about your emergency fund status.

Creating Your Personal Rebuild Protocol

Standard rebuild rules provide a framework, but your situation needs customization. Here's how to build a protocol that actually holds up under stress.

Step 1: Calculate your phase thresholds. Take your full emergency fund target and calculate the 30%, 60%, and 90% marks. These become your phase transition points.

Step 2: Determine your discretionary income. After essential expenses and minimum debt payments, what remains? This is your allocation pool for rebuilding and other goals.

Step 3: Set your phase allocations. Using the framework above, assign specific dollar amounts or percentages for each phase. Write these down — don't trust memory during stressful drawdown situations.

Step 4: Choose your automation method. Whether through banking apps, calendar reminders, or financial management software, pick your method and set it up now, before you need it.

Step 5: Document your triggers. List specific situations that trigger emergency fund use versus alternative funding. Be specific — "car repairs" is vague, "repairs required to commute to work" is actionable.

Step 6: Set review intervals. Schedule quarterly reviews to adjust thresholds and allocations based on income changes, goal shifts, or life circumstances.

The protocol document should fit on one page. If it's longer, it's too complex to follow during an actual emergency.

The Psychological Reality

Emergency fund rebuilds mess with your head in ways pure math doesn't capture. You feel like you're moving backward. You question whether the original expense was truly necessary. You wonder if the rebuild timeline is too conservative or not aggressive enough.

These patterns are predictable. The operational response is removing decision-making from the emotional moment through predetermined rules and automation. When the rebuild feels frustrating, you're not deciding whether to continue — you're following a protocol you established when thinking clearly.

The other thing worth knowing: rebuilding gets easier each time. Not because the math changes, but because you've proven the system works. The first rebuild feels like crisis management. The second feels like following a playbook. By the third, it's just temporary maintenance.

For those managing multiple financial scenarios, having clear rebuild protocols becomes even more critical for maintaining long-term stability.

Moving Forward

Emergency fund rebuild rules aren't about optimization — they're about sustainability. The best protocol is one you'll actually follow when stressed, tired, and frustrated about unexpected expenses.

Start with the basic framework: clear triggers, phased rebuilding, protection mechanisms for other goals. Customize based on your income pattern, debt situation, and psychological tendencies. Automate everything possible to reduce decision fatigue.

Most importantly, document your protocol before you need it. When you're staring at a four-figure repair bill, you want to execute a plan, not create one.

The goal isn't perfection. It's maintaining financial momentum even when life throws its inevitable curveballs. With clear rebuild rules in place, those curveballs become temporary inconveniences rather than permanent derailments.

Most importantly, document your protocol before you need it. When you're staring at a four-figure repair bill, you want to execute a plan, not create one.

The goal isn't perfection. It's maintaining financial momentum even when life throws its inevitable curveballs. With clear rebuild rules in place, those curveballs become temporary inconveniences rather than permanent derailments.

Ready to master your money?

Join thousands of users leveraging Savioly to build smarter budgets, save more efficiently, and plan for a secure financial future.