Getting a windfall feels incredible for about three days. Then the questions start. Pay off the car or invest? How much goes to taxes? What about that credit card debt you've been ignoring for two years?

Most people wing it. They pay off whatever feels most pressing, stick the rest in savings, and six months later wonder where half the money went. The other half? Usually sitting in a checking account earning nothing while credit cards charge 22% interest.

A windfall decision flow changes that. It's a systematic approach to allocating unexpected money—whether that's a $5,000 bonus, $50,000 inheritance, or $500,000 buyout. Specific percentages, immediate actions, and clear triggers for when to adjust the plan.

Why windfalls disappear without a system

Windfalls vanish through a thousand small decisions. You pay off the obvious debt first. Maybe the credit card. Then you start thinking about the car loan. A week passes while you research investment options. Meanwhile, the money sits in your checking account, slowly bleeding out through "just this once" purchases.

The psychological weight matters too. Large sums create decision paralysis. You know this money could change your financial trajectory, but that pressure makes every choice feel irreversible. So you make no choice—or you make all of them at once without any real coordination.

Tax surprises compound the problem. That $30,000 bonus becomes $21,000 after withholding. The inheritance you thought was tax-free triggers state inheritance tax. The stock options you exercised create phantom income. By April, you're scrambling to cover a tax bill from money you already spent.

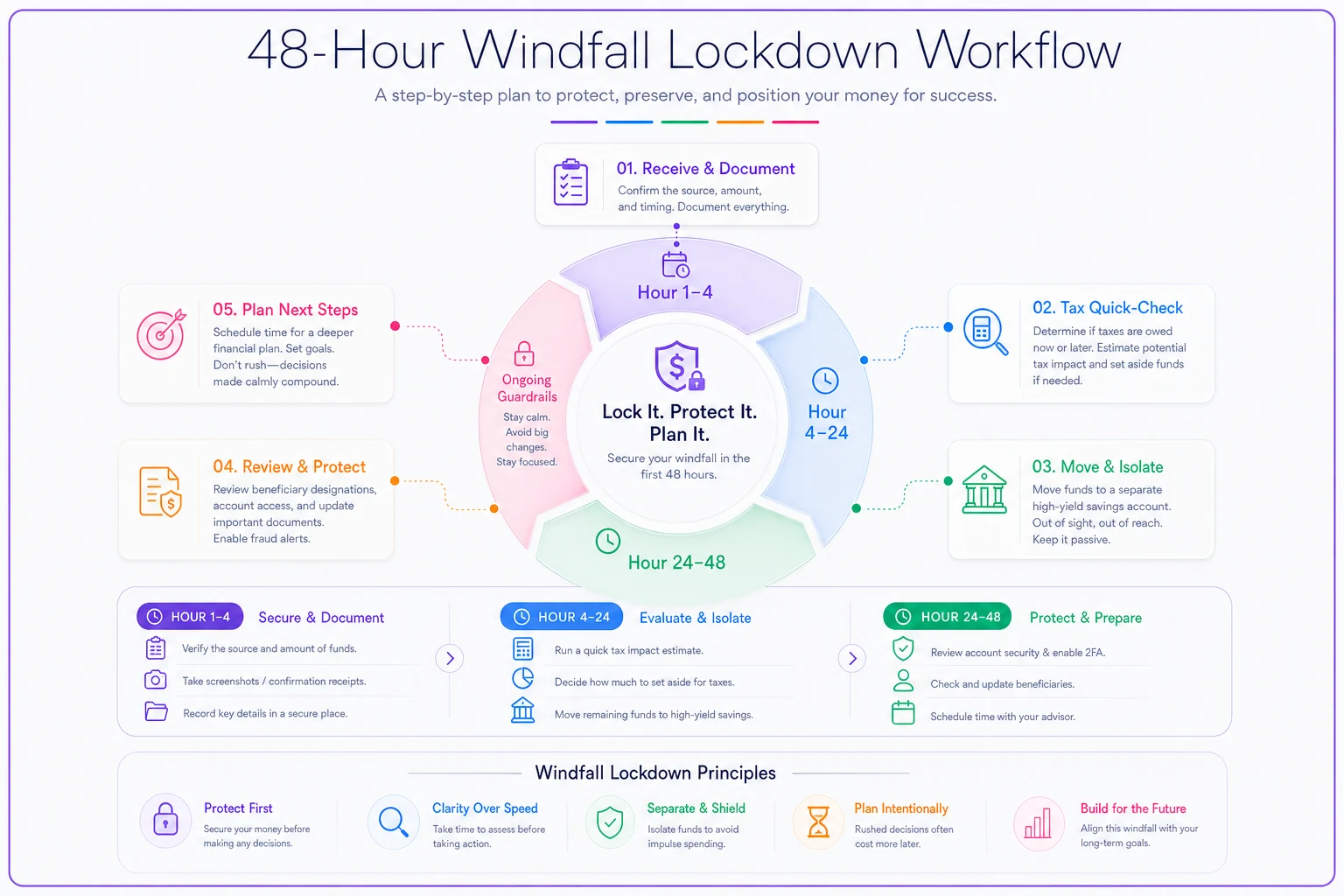

The immediate 48-hour lockdown protocol

The moment a windfall hits, implement a holding pattern. This isn't permanent—it's breathing room to make systematic decisions instead of emotional ones.

Take charge of your finances with clarity and confidence.

Savioly gives you real-time visibility and actionable steps to improve your money management.

- Automated expense tracking

- Goal-based saving plans

- Personalized financial insights

No credit card required

Hour 1-4: Documentation sweep

-

Screenshot or download the deposit confirmation

-

Note the exact amount and source

-

Check if any portion was already withheld for taxes

-

Identify any strings attached (vesting clawbacks, inheritance conditions)

Hour 4-24: Tax quick-check

-

Federal tax impact

multiply windfall by your marginal rate

-

State tax check

some states tax bonuses at flat rates

-

Quarterly estimate trigger

if windfall exceeds $5,000, you likely need to adjust

-

Special category check

inheritance, gifts, and insurance payouts have different rules

Hour 24-48: Create the quarantine

Move the entire windfall to a separate high-yield savings account. Not your regular savings—a completely separate account. This creates psychological and practical distance while you build the allocation plan.

A simple visual like this helps you follow the steps without digging back into instructions when the money arrives.

Core allocation framework by windfall size

The allocation percentages shift based on windfall size relative to your annual income. Small windfalls need focused impact. Large windfalls require more sophisticated splitting.

Micro-windfall (under 10% of annual income)

A $5,000 bonus when you make $70,000 annually needs surgical precision.

Allocation template:

| Category | Percentage | Notes |

|---|---|---|

| Tax reserve | 30% | Adjust based on your bracket |

| Highest-rate debt | 40% | — |

| Emergency fund | 20% | Until 3 months expenses |

| Immediate life improvement | 10% | — |

This concentrated approach maximizes impact. You're not trying to solve every financial problem at once—you're eliminating the most expensive ones first.

Standard windfall (10-50% of annual income)

A $30,000 inheritance when you make $80,000 requires broader distribution.

Allocation template:

| Category | Percentage | Notes |

|---|---|---|

| Tax reserve | 25% | — |

| Debt elimination | 25% | Highest rate first |

| Emergency fund boost | 20% | Target 6 months |

| Medium-term goals | 15% | Down payment, car replacement |

| Retirement catch-up | 10% | — |

| Immediate enjoyment | 5% | — |

The spread is wider here. You can address multiple financial layers without diluting the impact on any single one.

Major windfall (50-200% of annual income)

A $150,000 buyout when you make $90,000 transforms your financial architecture.

Allocation template:

| Category | Percentage | Notes |

|---|---|---|

| Tax reserve | 35% | Higher bracket likely |

| Complete debt elimination | 20% | — |

| Full emergency fund | 15% | 12 months expenses |

| Investment account | 15% | — |

| Retirement maximization | 10% | — |

| Life enhancement | 5% | — |

The tax reserve jumps because large windfalls often push you into higher brackets. This allocation also introduces real wealth-building categories beyond basic stability.

Transformation windfall (over 200% of annual income)

Anything beyond double your annual income requires professional coordination. The percentages matter less than the sequence and structure. You're not just allocating money—you're redesigning your financial life.

The 30-day implementation checklist

Days 1-3 — Tax and legal foundations

-

Days 1-3 — Tax and legal foundations - Calculate exact tax liability - Check for quarterly payment requirements - Verify inheritance tax obligations - Review gift tax implications if sharing - Consult a CPA if windfall exceeds $50,000

-

Days 4-7 — Debt hierarchy mapping - List all debts by interest rate - Calculate payoff amounts including early payment penalties - Check for tax deductions you'd lose (mortgage, student loans) - Run scenarios: full payoff vs. partial payoff + investment

-

Days 8-14 — Emergency fund right-sizing - Calculate true monthly expenses (not what you think you spend) - Adjust target based on job stability - Consider separate emergency fund for specific risks - Set up automatic transfers if not fully funded

-

Days 15-21 — Investment account architecture - Open brokerage account if needed - Research tax-advantaged options still available - Set up dollar-cost averaging for gradual investment - Avoid the "perfect timing" trap—systematic beats precision

-

Days 22-30 — Automation and safeguards - Set up automatic transfers for remaining allocations - Create spending rules for the "enjoyment" portion - Schedule quarterly review to adjust allocations - Build triggers for rebalancing if goals change

Build triggers for rebalancing if goals change

Scenario-specific adjustments

Work bonus scenario

Your company announces a surprise $12,000 bonus. Your salary is $65,000.

Tax reality check first: the bonus gets taxed at the supplemental rate—often 22% federal plus state. You're realistically looking at $8,500–9,000 in actual cash. Many companies withhold at higher rates for bonuses, so check your paystub carefully before you allocate anything.

Modified allocation:

-

$0 additional tax reserve (already withheld)

-

$3,500 to credit card debt (24% APR)

-

$3,000 to emergency fund

-

$2,000 to Roth IRA

-

$500 for something you've genuinely postponed

Inheritance scenario

You inherit $75,000 from a relative. Your income is $70,000.

Inheritance typically arrives tax-free federally—the estate already paid. But six states charge inheritance tax. Pennsylvania, for instance, charges 4.5% for direct descendants. Any earnings on inherited money become taxable immediately.

Modified allocation:

-

$3,500 state tax if applicable

-

$18,000 student loans (6.5% rate)

-

$20,000 emergency fund completion

-

$15,000 house down payment fund

-

$12,000 index fund investment

-

$6,500 home repairs you've been putting off

Stock option cashout

You exercise and sell vested options, netting $200,000. Your base salary is $110,000.

This triggers ordinary income tax on the spread, potentially pushing you into the 35% bracket. California adds another 12.3% on top of that. The tax liability here can genuinely blindside people who weren't tracking it throughout the year.

Modified allocation:

-

$90,000 tax reserve (critical—this could be higher)

-

$30,000 mortgage principal reduction

-

$25,000 college funds for kids

-

$30,000 backdoor Roth conversion

-

$15,000 next car purchase fund

-

$10,000 family vacation fund

This triggers ordinary income tax on the spread, potentially pushing you into the 35% bracket.

Replenishment triggers and reserve management

The tax reserve needs active management. Don't let it sit for 16 months earning minimal interest while you wait for tax day.

Quarterly checkpoint system:

-

Month 3

Verify tax calculations with actual income

-

Month 6

Pay estimated taxes if required

-

Month 9

Adjust reserve based on year-to-date income

-

Month 12

Final calculation and preparation

Reserve optimization tactics:

Park tax reserves in 3-month Treasury bills if the amount exceeds $10,000. You'll earn 5%+ while maintaining liquidity for quarterly payments. For smaller amounts, high-yield savings works fine.

Create automatic transfers. If you allocated $20,000 for debt payoff over 6 months, don't rely on remembering to move money manually. Set up $3,333 monthly automatic payments. This prevents the "maybe next month" drift that quietly kills allocation plans.

Park tax reserves in 3-month Treasury bills if the amount exceeds $10,000 to earn yield while keeping funds liquid for quarterly payments.

Build refill triggers. When your emergency fund drops below 80% of target, the next windfall—even a small one—goes there first. When retirement contributions lag, the next bonus gets diverted. These rules are what prevent lifestyle creep from absorbing every future windfall.

Common allocation mistakes that create long-term problems

The "house poor" trap: Dumping your entire windfall into a home down payment leaves you cash-poor. Houses need maintenance, repairs, emergencies. Keep at least $10,000 liquid after any major purchase.

The investment FOMO: Throwing everything into the market during a bull run feels smart until you need cash during a downturn. Follow the allocation percentages even when Reddit says otherwise.

The family loan disaster: "Lending" windfall money to family rarely ends well. If you must help, gift what you can afford to lose entirely, or create formal loan documents. Never lend more than 10% of any windfall.

The lifestyle inflation lock: Using windfalls to upgrade recurring expenses—bigger car payment, nicer apartment—creates permanent obligation from temporary money. One-time money should fund one-time expenses or permanent assets.

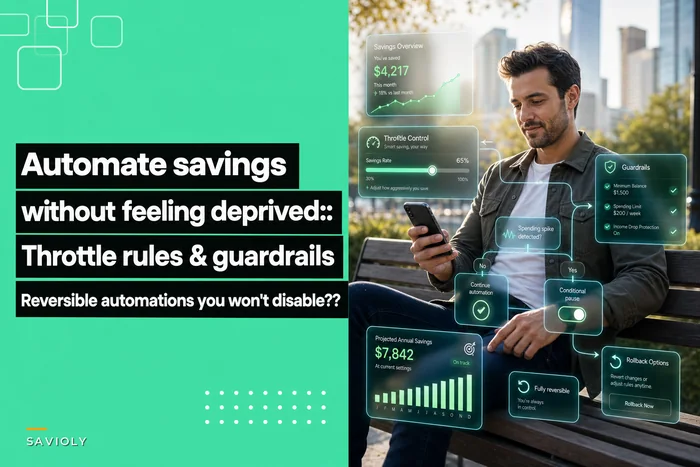

Digital tools that enforce windfall discipline

Modern banking tools can enforce your windfall decision flow automatically, preventing emotional overrides.

Set up dedicated accounts for each allocation category. Capital One lets you create multiple savings buckets. Ally Bank allows up to 30 savings accounts. Label them specifically: "2024 Tax Reserve" not just "Taxes."

Use apps that automate savings without feeling deprived. These platforms can split deposits automatically based on your allocation percentages—when the windfall hits, the distribution happens according to rules you set in advance rather than whatever you decide in the moment.

Investment platforms now offer automatic rebalancing and tax-loss harvesting. If you allocated $30,000 to investments, platforms like Betterment or Wealthfront handle the tax implications and maintain your target allocation without constant monitoring.

For people managing multiple financial goals simultaneously, AI-powered operational software can track where every windfall dollar goes. Instead of spreadsheets that go stale, these systems monitor your allocations actively, flag when reserves need refilling, and remind you about quarterly tax payments. The automation removes a lot of the mental overhead of managing multiple buckets—and it keeps things from quietly falling through the cracks.

Building your personal windfall playbook

Your windfall decision flow needs personalization. Start with the templates, then adjust based on your actual situation.

High-debt situation: If you carry credit card debt over 20%, increase debt allocation by 10% pulled from other categories.

Unstable income: Boost emergency fund allocation by 15% if you're freelance or commission-based.

Tax complexity: Add 5-10% to tax reserve if you have multiple income sources, side businesses, or stock compensation.

Track what actually happens with each windfall. Did you stick to the allocations? Where did you deviate? Most people genuinely get better at windfall management over time, but only if they're paying attention to what worked and what didn't.

Also worth noting: expense categories that actually change behavior matter here too. Your windfall allocations should align with your broader financial categorization system. If you track home repairs separately from general savings, your windfall should respect those same boundaries.

The compound effect of systematic windfall management

Five years of random bonus allocation might leave you with slightly less debt and a vague sense that money came and went. Five years of systematic allocation builds emergency funds, eliminates debt, and creates real investment momentum.

The framework also removes decision fatigue. When the next windfall arrives, you won't spend three weeks researching options. You'll execute your allocation template and move on.

Systematic windfall management also prevents regret better than anything else. You won't look back wondering where that inheritance went. You'll have clear documentation of exactly how it improved your position—each windfall becomes a step forward rather than a missed opportunity.

This isn't about perfection. Even following 70% of the allocation template puts you well ahead of the "figure it out later" approach that wastes most windfalls. Start with the next unexpected money that comes in—could be a bonus next month, could be a tax refund. Build the habit with small amounts, and when the large windfall arrives, the decision-making will already feel familiar.

Ready to master your money?

Join thousands of users leveraging Savioly to build smarter budgets, save more efficiently, and plan for a secure financial future.